Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Safe-withdrawal rates (SWRs) are perhaps the most extensively studied topic in financial planning literature. But applying a single SWR-driven methodology to all clients neglects their unique and individual needs. A better approach is for advisors to assist clients in defining their ideal and acceptable goals and the relative priorities among them. Then they can demonstrate through Monte Carlo simulation the likelihood of the recommended plan becoming over- or under-funded relative to those goals.

Much of the interest in SWRs has been driven by the aging and retirement-oriented demographics of the clients financial advisors serve. Advisors need some credible yet simple rules of thumb they can use to instill confidence and comfort in a decision that for the client is emotionally very scary and nearly irreversible: how to finance one’s retirement.

The notion of a SWR is simple. What can you “safely” withdraw in assets each year, adjusted for inflation over the course of your retirement, without leaving you with too high of a risk of running out of money before you pass?

William Bengen’s seminal 1994 article about the historical evaluation of a 4% withdrawal rate set the stage for this debate. Since then, many others have joined the discussion with various perspectives. Some claim there is a “new retirement” where people still work when they retire. Some have addressed the emotional fears retirees face by focusing on the risks, mainly of outliving one’s money, but sometimes advisors focus on these risks without considering lifestyle consequences or the size of the risk they are insuring against. Some advocate setting asset allocations based on one’s career being considered as an “asset.” Others have gained visibility by pointing out common-sense things that should be included in the calculation of sources of income (but excluded from the withdrawal rate calculation) to meet retirement spending needs like pensions, Social Security and even reverse mortgages. David Zolt suggested investors could have a significantly higher withdrawal rate (49% to 53% higher) if they forego inflation adjustments in years where returns are lower than the targeted returns along with other rules about asset allocation.

Embracing fears - Balancing reason and emotion

Put yourself in the place of a client who is contemplating retirement. On one hand there is an aspirational vision of pursuing those things in life you value, or regret having neglected. Be it golf, travel, fishing, or time with children or grandchildren, there is a pleasant aspirational vision of making the most of your life. On the other hand, there is also the fear that the income that has enabled your lifestyle will need to be replaced by assets for an unknowable amount of time. These conflicting emotions can provoke apprehension among retirees.

The fear side of the emotional equation includes the irreversible nature of retirement (considering the difficulty of getting rehired years later), visions of terrible capital markets that might leave you destitute, health-care costs that could surprise you at any time, and the potential expense for elder care like nursing homes or assisted living. No one is indifferent about the image these scary pictures paint. These risks are both real and emotionally taxing.

Financial services product manufacturers are aware of these emotions and have designed products to appeal to them. Many advisors use products like annuities, long-term care insurance or supplemental health insurance to allay specific fears clients express.

To deal with the fear of return-sequence risk, advisors bring other solutions to the table like a financial plan built through Monte Carlo simulations that provide a high degree of confidence. Advisors may also use the “buckets of money” approach, where near-term spending is funded through very low-risk (essentially cash-like) investments, while longer-term assets are deployed for growth to avoid needing to realize losses in the near term for spending.

Finally, there is the fear of inflation that can be appeased by the use of TIPS, various asset-allocation approaches using inflation hedges or inflation-adjusted riders on annuities.

Advisors are entrusted with the profound responsibility of guiding clients through the lifestyle they will have in their golden years that represents a lifetime of sacrifices to accumulate their wealth. It is critical that we listen to and understand these common fears. It is equally critical that we address them not just emotionally, but to help them understand the very real cost of insuring these emotions and risks. Our advice must balance the emotional understanding of the risks they (or we) fear while objectively assessing the consequences of such choices.

The beginning of Monte Carlo simulations

When online probability analysis tools for professionals started to appear back in 1999, some industry leaders were intrigued by the impact of return-sequence risk. Some were even in shock from the results. It was common for such tools to produce results that showed the client running out of money at age 76 with a trial in a simulation that had a 12% return, while another trial in the same simulation with a 9% return might provide money lasting through age 95 with a sizeable estate.

At the time, financial plans were generally built around conservative return assumptions for the underlying asset classes with zero variation in the year-to-year returns. This was unrealistic – even Treasury bill returns have a non-zero standard deviation. With it uncommon at the time to have tools to evaluate this, few practicing advisors were aware of the impact of sequencing risk. The bear market that began in 2000 highlighted the need to use tools that consider that portfolios can go both up and down, and the adoption of such tools increased.

Many of the first tools claimed that many financial plans would “fail,” even if the client experienced the assumed return, because of sequencing risks. The complexity of stress-testing plans a thousand times or more was simplified in reports and presented as a “success” and “failure” rate, terms that are still commonly used today.

What you call your results matters – Taking flight

Probability analysis is not a pass/fail grade. That isn’t how probabilities work and calling them pass/fail or success/failure is a mathematical and emotional misrepresentation of what is being calculated.

It isn’t odds of success, but odds of excess. When 830 of 1,000 simulations meet all of the client’s life goals and leave an estate value larger than the desired legacy goal, that is not an 83% chance of success . It is an83% chance of excess. The problem is that “success” implies only meeting the goals and assigns no value to the 829 of the 830 successful trials that exceeded the goals.

Think about the psychological and emotional perception from the client’s point of view based on the choice of words. You wouldn’t board an airplane that has an 83% chance of not crashing. Presenting the plan’s confidence level as a success rate creates the perception that the remaining 17% is failure… crashing, without even having to bring up failure rates.

Your clients pay a price by targeting too high a confidence rate. The words we use matter and if they emotionally scare people into comparing the “failure” of their plan to a plane crash, a comfortable journey versus nose dive, the result will be lifestyle sacrifice. We need to clearly communicate that it is not a simple pass/fail grade. Among the 83% “successful” flights are many that exceed expectations. They arrive hours early with first-class upgrades, complimentary sky cap service and a stretch limo waiting at baggage claim. While there is a valid emotional fear in worrying about outliving one’s assets, few clients would view a plan as “successful” for advice that caused them to sacrifice their only life to die on a death bed stuffed with money they wish they had spent.

Likewise, characterizing “failure” as being elderly and destitute overstates the reality of human behavior, emotions and common sense. Presume the markets are going through a Great Depression-like environment and there is 25% unemployment. Your neighbors are waiting in soup lines. Ten years ago, though, you built a financial plan that had 83% confidence of exceeding your goals but you are experiencing some of the 17% of the simulations that had you “fail.” But those “failing” trials assumed you spent three weeks a year at a luxury resort in Jamaica. Do you think you might cut it back to only one or two weeks in such an environment?

It isn’t odds of failure or crashing; it is the odds of needing to get off the plane before it crashes.

Correcting the path before a crash is imminent is a value proposition advisors can deliver. The research about spending rates for average or ranges of client types gives us good academic fodder. But few of the rules inherent in those analyses will enrich the life of any one client. We might convince our clients to follow the assumptions in any of the various spending rate approaches, but that does not mean we have necessarily made the best choices for any one client. To deliver that, we must set expectations in advance for change (course corrections). Advisors and their clients need to calculate and establish the points in our future path that would trigger such a change, and we need to understand and agree to in advance the range of the ideal and acceptable goals and priority of the choices among them based on each unique client (passenger).

Failure rates convey a concept similar to our plane-crash analogy even though financial plans are much different. We fear a failed flight for a lot of reasons, mostly because we are out of control and there is nothing we can do. You cannot get off a failed flight; you are going down with the plane. That is what clients perceive as the “failure rate” of a financial plan.

But it is not analogous to the analysis we do. If you are on a roadway in your life-long financial journey and you are veering off course, there might be 17% of the trials where you would crash if you ignored that fact. But unlike planes, plans can be changed to avoid most of those 17% outcomes. It might be stressful, like a pilot experiences in an evasive maneuver or a more modest inconvenience like reaching an alternative nearby landing site.

To many investors, the term “failure rate” does not convey that they have the choice of getting off the plane…or plan.

The over/under odds

Monte Carlo simulations encounter two primary problems based on how they are normally used and the words chosen to convey their results. One is the very real risk of running out of money if the plan never changed despite the markets. The other is the lifestyle price of the extreme sacrifice that would be needed to eliminate those scary “odds of failure.”

By tying the output to the goals of the client, such simulations shed an obvious light on the price of living your life planning for some of the worst environments. Those simulations show that to have high confidence, you need to sacrifice your lifestyle now by increasing your savings to such a level so you won’t have to worry about the risk of eating cat food in retirement by getting you used to the taste of it right now.

Monte Carlo simulation can be much more useful than merely measuring life-long success and failure rates. In fact, if the highest success rate is all one is targeting, you don’t need Monte Carlo simulation; you can assume the client gets no return or that they lose all of their money. The real value from Monte Carlo does not come from knowing whether you are saving too little and risking failure, or spending too much and not taking enough risk. Instead, its value is to allow advisors to be balanced and also communicate the consequences of under-spending, taking needless risks or over-saving.

Our approach to planning changes when we view it as a tool to measure the point in the uncertainty distribution of outcomes of becoming either under- or over-funded, with the odds tilted sufficiently to have reasonably high confidence.

Rethinking the approach to planning

To make the most of your client’s only life, advisors have to become skilled at balancing emotion and reason, neither to the exclusion of the other.

As an industry, financial professionals have no shortage of experts claiming that people are not saving enough or are spending too much. Nor is there a shortage of those who use financial products to insure against those fears, target very high confidence levels in simulations or engineer sub-optimal spending plans to avoid selling at a loss. In the absence of defining when “conservative enough” crosses into the territory of needless or irrational sacrifice, insuring or hedging risk of any size becomes the priority and “safety first” trumps the lifestyle of the client… the price being their lost dreams, compromised choices, and a life left without being enriched by what they value. The cost of needless conservatism needs to be understood, measured and communicated.

Pensions can be over- or under-funded – Why not financial plans?

Think about how the perception of pension plans has reversed over the last 25 years. In the 1990s, pensions, with their conservative actuarial assumptions, were passé compared to the soaring returns people were getting in 401(k)s. In the last decade or so, some of the weakest capital-market returns in history reversed that perception. PBS even produced an expose on the topic, The Retirement Gamble, providing a nostalgic view of the days when someone would spend their entire career at a company to retire with a gold watch and a pension that would last their lifetime.

People naturally like the comfort and “guarantees” of things like pensions or annuities except when they realize they are giving up significant upside that could have improved their life.

Wouldn’t the ideal retirement plan be one where you could have the same or similar confidence as a pension plan yet still get the upside should the markets perform well? That is what I propose. The problem isn’t that we need guaranteed income products added to 401(k) plans or more defined-benefit plans where the company gets the upside of strong markets instead of the beneficiary; instead we need to compare the two on an apples-to-apples basis by including over- and under-funding status of 401(k) participant balances relative to their goals.

It is important not to over-estimate how confident you can be in a pension promise. Pensions have a reasonably high confidence of paying the promised pension but that does not mean that pension beneficiaries can be certain they will never have to adjust their plan. How many plans have you heard of that were frozen or stopped accruing future benefits? Even those that are taken over and guaranteed by the Pension Benefit Guarantee Corporation (PBGC) only had 80% confidence in delivering the promised benefit.

Currently, 4,400 private-sector pension plans have been taken over by the PBGC, and 20% (280,000 out of 1.4 million) of participants were forced to accept a reduced pension. Sounds like a change in plans to me, and similar to our targeted confidence levels.

If you can target sufficient confidence as in a pension plan, you can have similar comfort in your retirement income. The difference is instead of the company getting the benefit of market upside, you get it to improve your life and potentially reach some of your ideal goals and dreams that would otherwise be lost with the guarantee of a pension or annuity.

People like choice and safety – Can they get the best of both?

While there are a litany of well-researched approaches on the topic of SWRs (e.g., using insurance products with guarantees, rules that waive inflation adjustments in below-normal years, modeling longevity far longer than clients would likely ever experience, asset-allocation models to hedge inflation or optimize results, and Monte Carlo simulations with high confidence of being exceeded), the academic validity and practical value of such methods would be enhanced by incorporating a few rules of communication:

- Balanced context and relativity in communication;

- Set expectations that the plan will need to change;

- Show the future values that would trigger a change;

- Disclose the odds that the plan will need to change in the near-term, not just long-term, since that is when we need to deal with clients…it is too late if they are at their mortality age or already broke; and

- Set ideal and acceptable goals and understand in advance the relative priority among those goals so that when uncertainty presents itself we are prepared for what course of action we would take for each specific client. That set of choices will be customized to each client’s priorities, unlike the generic rules of thumb used in much of the academic spending rate approaches.

Let’s look at each of these five imperatives.

Balanced communication

In making sure that context and relativity is balanced and clearly communicated, our choice of words matter. I already explored what a client might perceive from the use of “success” and “failure” rates and how Monte Carlo simulation can be morphed to convey over- and under-funding status, just like a pension.

There are many other examples of needing to choose our words carefully and balancing context and relativity. For example, while it may be true that a single-premium immediate annuity (SPIA) guarantees an income for life, it should not be ignored that an SPIA may not be an advantageous bet for the buyer of the product. In a recent article about optimizing portfolios using SPIAs, an example used a couple and a (presumed) joint-life SPIA in portfolio optimization calculations. The SPIA returns were calculated with a joint-life mortality table provided by David Hulstrom and posted on Michael Kitces’ website. Table 1 shows the percentage return of the product at a few sample mortality ages, and the percentage of buyers that would do worse than these results based on the joint life mortality.

Table 1 – Returns and percentage of buyers that would do worse at different mortality ages:

In making an informed decision on the SPIA, both the benefits of the lifelong income guarantee and the opposite side showing the percentage of buyers doing worse should be presented objectively and fairly. Both should be acknowledged but balanced so that emotional fears do not lose the light of reason.

The SPIA has essentially no chance of doing any better nor worse than the returns in the table at specific mortality ages. That is the choice. Presenting the SPIA with both the emotional benefits it delivers yet showing the reasoned reality of the returns it would deliver and the odds of how many buyers would do worse than that at various mortality ages would have the client (or even the advisor) rethink a decision that might overweight the emotional fear the annuity is designed to target.

Setting an expectation for change; Showing future values that would trigger a change

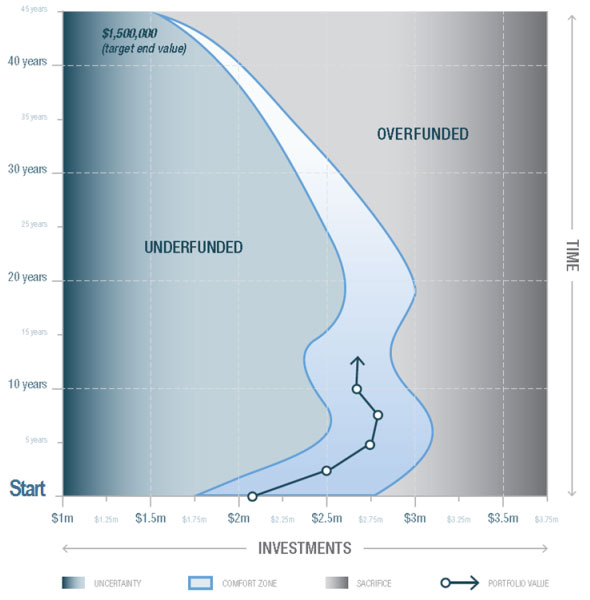

Any plan based on a Monte Carlo simulation will need to change to be consistent with the premises of the targeted confidence or comfort zone of the original recommendation. Depending on the degree of confidence targeted, the odds may be tilted toward having a higher chance of course corrections resulting in improvements in the client’s lifestyle, rather than compromises. Figure 1 is an example of the road map for how Monte Carlo simulation can be used to convey the future values that would trigger a change in the plan.

Figure 1 – The Roadway or Path to Navigate for a Life Long Financial Journey:

This roadway (or “Wealthcare Way™”), was produced with my company’s Financeware software, for a sample client who started their journey 14 years ago with a 45-year plan. This “road map” makes it easy to understand the future (and past) portfolio values that would avoid being either over- or under-funded. The horizontal axis represents the value of one’s assets, and the vertical axis shows time, progressing from bottom to top.

The turns in the road can be caused by either extreme cash flow goals in the past or future, or by changes that were made in the plan in the past in response to over- or under-funding due to market movements, changes in goals or priorities discovered in ongoing reviews, or unexpected positive or negative cash flows (same effect as a market movement going forward). The line with dots tracks where you’ve been on your way, the arrow represents where you are today and the comfort zone path shows the range of where you need to be in your life-long journey for your current plan at any given time in the future.

To deal with the near-term for clients who have regular reviews of their plan, advisors can zoom in on just the last year or two and next three or so years to show the range the portfolio needs to be within to stay on course. Table 2 exposes the need for ongoing advice from the advisor by showing the odds that the plan might become over- or under-funded, triggering a course correction.

Table 2 – Short-term excursion – Odds the plan will need to change

|

Odds of Under Funding

|

Odds of Being In Comfort Zone

|

Odds of Over Funding

|

Odds of Needing a Change in Course

|

|

Next Five Years

|

18.5%

< $2.5 Million

|

49.1%

> $2.5 but < $3.0

|

32.4%

> $3.0 Million

|

50.9%

|

|

Next Three Years

|

14.0%

< $2.4 Million

|

67.9%

> $2.4 but < $2.8

|

18.1%

> $2.8 Million

|

32.1%

|

|

Next Year

|

4.2%

< $2.3 Million

|

82.3%

> $2.3 but < $2.8

|

13.5%

> $2.8 Million

|

17.7%

|

This application of Monte Carlo simulations bridges many gaps. Remember that many Monte Carlo simulations show results only over the life of the plan, and trials that became over- or under -funded along the way are ignored for veering off course. All that usually matters is the ending outcome in the typical success/failure analysis. In the example shown in Figure 1 and Table 2, the client has nearly a 51% chance of needing a change of course due to market movements alone within the next five years. The plan had 83% confidence of exceeding the goals over the client’s life. Shedding light on the higher near-term odds that the plan will need new advice allows advisors to set realistic expectations and prevent needed changes from being viewed as surprises.

Boy Scout planning – Being prepared with ideal and acceptable goals and priorities

Setting the expectations for the likelihood of the need to change a plan in the near term is a wasted teaching moment if advisors are unprepared – without the information such as Figure 1 and Table 2. In the absence of such preparedness, the excitement of soaring markets and portfolio values can trigger excessive optimism and potentially reckless spending. It may lead clients (or advisors) to increase portfolio risk at a time when the client has won the market lottery and could afford to take less risk. The reverse is true; devastating bear markets could cause the client to make needless sacrifices to his lifestyle or reduce portfolio risk when increasing it might be the best choice. This analytical framework forces advisors to focus more on emotion of what the client truly values .

Getting clients to identify ideal and acceptable goals in the discovery session and ongoing reviews is easier than asking them to pick a single value they might be flexible about. It also has clients agreeing in advance to the range of boundaries so that the advice the advisor gives can meet or exceed acceptable values instead of the advisor having to negotiate goals downward from a single fixed value. Psychologically, it is a far more positive experience to hear your travel budget is $5,000 more than what you said was acceptable instead of $10,000 less than what you wanted. Understanding the priorities and tradeoffs that clients are willing to make, in time or size for their goals, is common-sense preparedness for coping with market uncertainty.

Advisors can ask several questions to facilitate this process. What would be the first goal you would adjust if you became over-funded? Would it be moved sooner, increased in size or last longer? Or, would there be modest adjustments to multiple goals? If you became under-funded, what goals would you compromise, delay or modify first to make the needed course correction?

Do not forget risk

Capital-market risk exposure should be part of these discussions, choices and priorities. In practice, it is best to avoid positioning the client at his or her maximum tolerance for risk. Usually, advisors need to make very minimal adjustments in the recommended goals for a plan that is a notch below a client’s risk tolerance. Having room to increase risk is valuable in dealing with market uncertainty.

Conclusion

There are many valid and well-researched strategies for determining SWRs. But the SWR-driven approach masks the need for advice that is customized to the needs and desires of each individual client. Some clients have priorities that differ from the rules used in many of SWR strategies, leaving the door open to advisors to adopt an approach using these strategies while applying a consistent, balanced and objective method of communication to meet all client needs.

Embracing emotion, applying reason, being prepared, setting expectations for the likelihood of change, communicating a simple road way (or Wealthcare Way™) showing where you have been and where you are going, instills comfort and confidence. Showing the lifestyle prices of various choices demonstrates objectivity and interjects the opportunity to educate clients about the consequences of irrational and emotional decisions, not by squelching emotion, but by embracing what the client truly values.

A popular industry speaker, writer, consumer advocate and inventor, David B. Loeper is the CEO and founder of Wealthcare Capital Management, Inc. in Richmond, VA. He is author of the top-selling book Stop the 401(k) Rip-off!, three other books released by John Wiley & Sons (Stop the Retirement Rip-off, Stop the Investing Rip-off and The Four Pillars of Retirement Plans) and numerous whitepapers. He has appeared on CNBC, CNN, Fox Business and Bloomberg TV, served on the Investment Advisory Committee of the $30 billion Virginia Retirement System and was chairman of the Advisory Council for the Investment Management Consultants Association (IMCA). Before founding his company in 1999, he was Managing Director of Strategic Planning for Wheat First Union. He earned the CIMA® designation (Certified Investment Management Analyst) from Wharton Business School in 1990 in conjunction with IMCA.

Read more articles by David B. Loeper