Adapting the Yale Model for Clients

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Yale University endowment fund is one of the most successful in the country, with a 10-year return besting the endowment universe average return by 300 basis points and the Wilshire 5000 return by 400 basis points. David Swensen is the architect of this program, and his guiding principles are widely used to manage large endowments. They are equally useful for client portfolios.

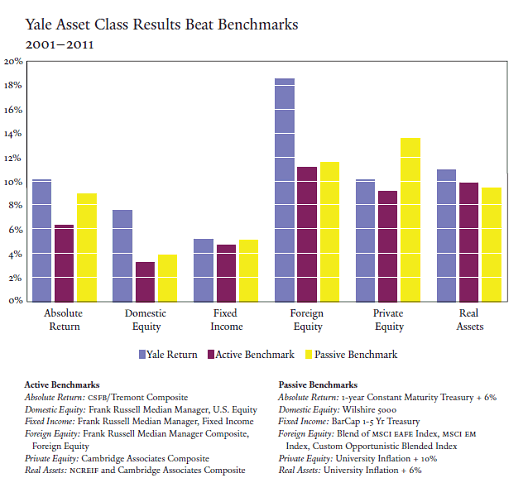

Swensen has written extensively about the approach used by Yale to construct portfolios and hire asset managers. In simple terms they make better asset allocation decisions and hire better investment managers. The results are provided in the table below.

Several pillars undergird Swensen’s approach, and can be used by advisors in what we call the “Personal Endowment Model”:

- Separate short-term and long-term investment buckets,

- Careful strategic allocation, and

- Select superior active managers.

Creating investment buckets

One of the more difficult challenges faced by investors is removing emotions from investment decisions. This is particularly critical at the overall portfolio level, where emotional decisions can significantly impair long-term wealth. History reveals that moving money in and out of investments when responding to highly emotional events is a poor way to grow long-term wealth. On the other hand, short-term investments play an important role in constructing a prudent reserve or emergency fund as well as providing an operating fund for meeting income needs.

It is critical to divide the portfolio into three investment buckets:

-

Emergency fund/short-term income bucket

This pool of money covers emergency needs as well as provides short-term income. It is insulated from market volatility by means of investing in savings, CDs, money market instruments, or short-term notes. Investors must know that these needs are taken care of regardless of what the market does. Consequently, volatility has been removed as an emotional trigger.

-

Capital growth bucket

This pool of money builds long-term wealth. Investors do not have the infinite time horizon of endowments, but the majority of investors do have very long horizons. Those in their 20s, 30s, and 40s face long horizons as life expectancy grows ever longer (when he taught at the University of Denver, Tom would say to his undergraduates that their investment horizon was maybe 80 years, a point that was often met with a scowl!). Even those who have recently retired face a long horizon. For example, Tom recently retired from the university. He and his wife have a joint life expectancy of 30 years, the same length of time that he taught at the university.

In addition, Tom has set up trusts and foundations which will exist at least 20 years after he and his wife are gone. They use a 50-year time horizon for building their capital growth portfolio. While 50 years is not forever, for practical investment purposes it is and so it makes sense to think of this portion of the portfolio as an “endowment”.

The most important determinate of long-term investment performance is expected market returns and so the capital growth portfolio should be largely invested in those markets with the highest expected market returns. For example, if you agree that stocks provide among the highest expected returns (the stock market has produced an average 10% compound annual return over long time periods), then stocks should play a prominent role in this bucket. The primary consideration for including an investment in this bucket is the magnitude of its expected return. Other factors, such as volatility, should be secondary, since long-term capital growth is the primary objective.

By taking a long-term view, the importance of volatility and correlation diminish. The short-term benefits of volatility reduction as well as the returns available from most low correlation investments shrink when building long-term wealth. In this context, the current infatuation with alternative investments (such as commodities, real estate, hedge funds and private equity) can be harmful to building long-term wealth, as they often provide lower volatility and lower correlations at a significant reduction in expected returns. One must understand the premium being paid for these secondary benefits.

Remember, the goal is to build long-term wealth. Unfortunately this comes with emotionally charged short-term volatility. But, short-term volatility is relatively unimportant in the performance of long-term capital portfolios.

As we know all too well, emotions often override the most carefully constructed logical argument. This is where a conscious decision has to be made to remain focused on the long-term. The cost to do otherwise is steep. For example, investing $10,000 in stocks in 1951 and remaining fully invested in this volatile market over the 62 years through 2012 resulted in a portfolio worth $5.2 million versus a $0.4 million portfolio invested in less volatile bonds. This decision cost $4.8 million!

You can always look backward and find short time periods when other investments have outperformed stocks, but it is what we expect going forward that matters when building portfolios. The highest expected return market(s) should dominate the capital growth bucket.

In this approach, for both the emergency/short-term income and the capital growth buckets, the importance of market volatility is much diminished. In the former, the portfolio is constructed to avoid volatility entirely, while in the latter the focus is on long-term expected returns and not on short-term volatility. It is best to view volatility as an emotional issue that, through careful portfolio construction and disciplined decision making, can be sidetracked as an ongoing investment concern.

-

Non-standard bucket

Most investors have some assets that do not fit into one of the first two buckets, such as annuities, their primary residence and other real estate, a long favorite stock, precious metals, and collectibles. These are generally managed quite differently than are the other two buckets and are often held for reasons other than short-term liquidity or long-term growth. The idea is to segregate these from the remainder of the portfolio and manage them as appropriate.

Creating three investment buckets allows each to be built and managed to meet the investor’s specific needs, rather than simply allocating the portfolio to the traditional 60/40 stock and bond mix or an arbitrary basket of investments. The investor and advisor can determine the right mix in each bucket to meet their needs. This approach has the important advantage of sidelining volatility as an investment issue.

Strategic asset allocation

Rather than simply investing in broad asset classes, endowments make strategic decisions to pursue specific strategies. For example, Yale’s private equity program is regarded as among the best in the institutional investment community. Since inception, private equity investments have generated a 30.3% annualized return to the university. Yale generated these strong returns in private equity with a few high-conviction investments. More recently they have generated impressive results in foreign equity with carefully selected managers and country exposure.

Individual investors and their advisors can make similar decisions to allocate among attractive strategies. The keys here are that simple 60/40 allocations no longer function as they have in the past, style boxes are not investment strategies, and portfolios of global mush with hundreds of tiny positions have little chance of outperforming. Endowments build strategic positions and hold them for significant time periods, even sacrificing liquidity at times in exchange for returns.

Few advisors should pursue private equity investing, because that requires extensive due diligence and expertise. But they can pursue focused investing strategies within the realm of publicly-traded funds.

Excess returns matter

Within the capital growth bucket, it is important to earn excess returns. For example, a 4% excess return (the excess return earned by Yale over the last 10 years) on top of a 10% expected return generates an additional $3,000,000 for each $1,000,000 invested over a 30-year period. Excess returns matter over long time periods. Passive indexing yields the market return, at the lowest possible cost, while successful active managers can provide excess returns. So it is important to identify truly active managers for each investment used for capital growth.

Identifying truly active managers

Swensen specializes in identifying truly active managers over a wide range of assets. He is a believer in first identifying asset classes where active management has the best chance of outperforming. For example, he believes that government bonds offer neither attractive expected returns nor good opportunities for earning excess returns. On the other hand, equity markets offer a wide range of both expected and excess returns. The key is to build a capital growth portfolio comprised of investments with both high expected returns and the potential for high excess returns.

There is a compelling stream of research that supports the fact that excess returns can be generated over the long-term by active equity managers. The first step is to separate truly active managers from closet indexers. Unfortunately the active equity fund mutual fund category is widely populated with bloated funds that hug their benchmark. Low R-squared and high active share are useful tools in identifying truly active managers within this group.

Second, one must understand the investment strategy being pursued by a manager as well as their level of consistency and conviction. The best active managers consistently pursue a narrowly defined investment strategy. A manager’s strategy zeros in on aspects of the market that they believe produce superior returns and allow the manager to rank investment opportunities. A manager’s stated investment strategy can be found in the prospectus. The old adage “Read the prospectus carefully” applies when evaluating managers.

After managers analyze the full range of investment opportunities based on their strategy criteria, the good ones heavily invest in their best ideas. High-conviction positions are an important aspect of a successful active portfolio management. The relative weights, rather than absolute weights, of positions within a portfolio are what define a manager’s level of conviction.

Truly active portfolios look very different than their benchmarks. They experience higher short-term volatility and display high tracking error. They both underperform and outperform the benchmark by wide margins in the short run. As a result short-term return performance measures and benchmarking provide little help in identifying successful active managers.

Instead, the best way to identify good managers is to focus on manager behavior: strategy, consistency, conviction. Every effort should be made to determine if the manager continues to consistently pursue a narrowly defined strategy and continues to take high conviction positions. Past performance is an unreliable indicator of such desirable behavior.

A personal endowment model

Since most investors face a long investment horizon, it makes sense to build a portfolio to take advantage of what made Swensen and the Yale endowment so successful.

First, create three investment buckets: 1) emergency fund/current income, 2) capital growth, and 3) non-standard. Each is intended to meet different needs and thus is managed differently. A side benefit of the three bucket approach is to reduce the importance of short-term volatility in managing the overall portfolio.

Second, the capital growth portfolio should be concentrated in a reasonable number of asset classes with the high expected and excess return potential.

Third, to find the best active managers, focus on manager behavior – investment strategy, consistency, and conviction – and not on volatility, tracking error or past performance.

Investors can comfortably meet short-term needs, while at the same building long-term wealth, as Yale and other endowments have done so successfully over the years.

Tom Howard is CEO and director of research for Denver-based AthenaInvest and professor emeritus at the University of Denver. Lambert Bunker is the vice president of business development for AthenaInvest.

Read more articles by C. Thomas Howard, PhD and Lambert Bunker

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All