Count Jeffrey Gundlach among those who expect Japan’s currency to collapse because it can’t service its debt. Japan’s challenges may parallel those that the US faces, and Gundlach feels strongly that they have created a compelling investment opportunity.

Speaking a day before Federal Reserve Chairman Bernanke announced that the Fed would step up its quantitative easing policies, Gundlach warned investors that such efforts would have diminishing returns. Near-zero interest rates and an expansion of the Fed’s balance sheet won’t boost asset returns, he said, and they don’t address the fiscal imbalances our country faces.

“We’re in this predicament owing to a simple fact,” Gundlach said. “The United States has been spending more than 50% more than it’s been taking in in taxes. “ Addressing the budget deficit will be costly, he added, and an “instant recession” will ensue if deficits are reined in too quickly.

In Japan’s case, meanwhile, Gundlach said quantitative easing will have far more insidious effects – most notably, debasement of the yen – and that creates opportunities for investors.

Gundlach, the founder and chief investment officer of Los Angeles-based Doubleline Capital, spoke to investors in a conference call on December 11. The slides from his presentation are available here.

I’ll discuss Gundlach’s high-conviction investment idea in more detail, but first let’s review his assessment of the economic landscape – including the fiscal cliff – and his outlook for Japan, which may prove to foreshadow the fate of the US economy.

A challenged US economy

“Clearly, people don’t want to see the economy contract very substantially next year,” Gundlach said. “But, as I’ve said for several years now, addressing the budget deficit equals economic weakness and headwinds, and perhaps if it’s addressed aggressively, that’s just instant recession.”

Gundlach was very skeptical that progress would be made to avert the fiscal cliff, much less toward addressing the larger deficit issues. The fiscal cliff negotiations have been unable to bridge gaps as small as $70 to $80 billion annually in tax increases, he said, which does not bode well for addressing the $1.3 trillion deficit.

“Ultimately, you must balance the budget,” he said. “To do that, you have so much more work to do than this tiny little issue about 2% of the population.”

Lack of progress on the fiscal cliff has impeded growth, according to Gundlach, by delaying businesses’ decisions about spending. Confidence among corporate leaders has “plummeted,” he said, since reaching a fairly high level in the first part of 2011, and the data show that purchases of equipment, software and other goods have been very slow lately.

Higher taxes are likely, according to Gundlach. He warned that other states may follow the example set by California in the recent election; it raised taxes by 30%, retroactively, on its wealthiest citizens. He also said that more granular tax brackets were probable, such as additional brackets at $500,000 or $1,000,000.

“It’s possible that taxes on the very wealthy in America could go very, very substantially higher, because there really is no resistance to raising taxes on the wealthy,” he said.

At the other extreme, Gundlach said that most of the jobs gained in the current recovery have been low-wage. As a consequence, he said, median household income has fallen in real terms since 2000, and in nominal terms it is below its 2008 peak.

Labor-force participation has spiked for workers over age 75, who have seen their wealth depleted and can no longer live off their savings, Gundlach said. Their incomes have grown slightly, but the economic hardship is worse for the younger generation. Unemployment among teenagers has increased sharply, making it extremely difficult for them to get jobs, he said.

The message from Japan

The two-decade miasma of slow growth and fiscal imbalances that Japan has endured are a cautionary backdrop for US policymakers as they grapple with these challenges. Gundlach had not discussed Japan in previous conference calls, but this time he drew a number of parallels between its situation and the US’s.

Gundlach’s analysis of Japan closely resembled that articulated by the hedge-fund manager Kyle Bass in a talk a month ago at a University of Virginia conference.

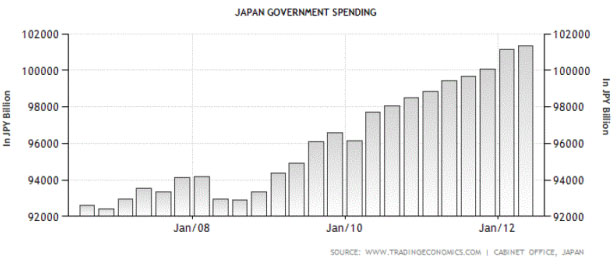

With debt more than double its GDP, Japan is far more indebted than the US and still headed in the wrong direction. According to Gundlach, Japan’s debt has increased by half its GDP in just the last four years.

“Government spending, of course, is what’s responsible,” he said, and presented the data below showing the persistent rise of quarterly spending:

Japan’s rising imports – exacerbated most recently by demand for new, foreign energy sources since the 2011 tsunami and nuclear disaster – have created a trade deficit, Gundlach said. Its aging population is further depressing Japan’s current account, he added, forcing it to engage in increasingly aggressive monetary policies.

“Japan should be watched for moving into an inflationary exercise,” he said. Japan is out of policy tools, according to Gundlach, and will “embark first on an exercise in debasement in an attempt to create inflation.”

Japan may still have room to lower its interest rates, since, unlike in the US, real rates remain positive in Japan.

The potential for lower interest rates carries a message for those who expect high-dividend stocks to outperform bonds. Gundlach noted that, at the end of 2009, Japanese stocks had higher yields than Japanese government bonds. Yet, those bonds have outperformed stocks since then. Gundlach did not predict the same outcome for US investors, but he said there’s “no guarantee that just because a certain stock portfolio might have a higher dividend it would outperform even a government bond portfolio.”

A high-conviction investment idea

One of Gundlach’s “most high-conviction investment ideas” stems from his assessment of Japan’s economy. The likelihood that Japan will ease monetary policy means that investors should short the yen versus the dollar – or even the euro – he said.

Those investors should also go long the Japanese stock market, which is something that Gundlach has not previously recommended. Debasement, he reasoned, would spur exports and benefit Japanese industries.

“I wouldn’t be surprised if the Nikkei, which has risen about 10% or so from its low just a month ago, found its way higher by a couple or even three thousand points during the year 2013,” he said.

Gundlach also noted other investment opportunities, for which his degree of conviction was somewhat lower.

The Shanghai is cheap, he said, particularly relative to the S&P. It would serve as a good hedge against the possibility of a “disaster” in the global economy, or it would do well if inflationary policies lead to broad market rallies.

Investors should be careful with emerging markets until food prices stop rising, Gundlach said, because in those economies food is an exceptionally large part of the average household’s budget.

Gold has generally fared well during this era of global quantitative easing, Gundlach said, a relationship that he considers “fairly convincing and fairly logical.” “If you’re thinking of QE forever and QE on a coordinated basis coming more and more,” he said, you should favor gold over stocks.

In the US, Gundlach said, Fed purchases of mortgages have made prices in the non-agency market “incredibly unattractive,” and he is looking at “certain other sectors that are less affected by the negatives” of the Fed’s program.

Gundlach said he has been negative on mortgage REITs for the last several months, since it became evident that Fed activity would lead to increased prepayments on the underlying securities. He expects dividends to be cut on REITs, which would cause prices to decrease.

Interest rates have bottomed in the US, Gundlach said, reiterating comments from his previous conference call. The bottom for the 10-year Treasury note was 1.39% on July 24. Volatility in the fixed-income markets was low in 2012, but he expects it to pick up next year.

Nor will interest rates in the US move sharply higher. Gundlach said the Fed could keep interest rates low for an indefinite period of time, through open-market purchases of bonds. He said the Fed would continue to expand its balance sheet in 2013.

Gundlach said he expects the return on Doubleline’s Total Return Fund (DBLTX) for 2012 to end up slightly more than the 8% to 9% he forecast at the beginning of this year. For next year, he said he hopes the fund will return 6%.

Read more articles by Robert Huebscher