Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In the investment business, assets under management are concentrated with the largest and most established firms. Understandably, investors tend to allocate capital to managers after they’ve established a good track record. Unfortunately, for many, the analysis stops there. By failing to separate good results from identification of what makes a great investment manager, investors are primed for disappointment.

I recently came across a Fortune Magazine article from 1989 titled Are These The New Warren Buffetts? The article attempted to identify which of the then-current cadre of young money managers might “go on to investing fame and their clients to fortunes.” Of the 12 managers highlighted in the article, 10 were in their 30s, and most only had independent track records of one to five years. Despite this, though, the article attempts to identify what makes a great money manager capable of delivering superior returns. The article provides an ex-ante assessment of what most investors only analyze ex-post.

Now that we have 22 years of history from which to judge these managers, we can evaluate the effort.

The Fortune article cites Warren Buffet, who prioritizes “high-grade ethics. The investment manager must put the client first in everything he does.” He said he wants to know that a manager handles his mother’s money as well as his clients’. Intelligence is important, but the proper temperament is essential: “Rationality is essential when others are making decisions based on short-term greed or fear,” Buffett said. “That is when the money is made.” While the article follows managers who invest across a variety of asset classes — both long and short — and utilize a variety of strategies, the common thread is a value discipline in the spirit of Buffett’s mentor Benjamin Graham. They all use fundamental analysis, among other things, to find mispriced securities that offer a margin of safety. Importantly, the all seek to minimize the true risk of investing—a permanent loss of capital.

The list of 12 managers is astounding, in that it presciently identifies many of the most prominent and successful managers of the last two decades: Michael Price, Jim Chanos, Karen and Jim Cramer, Glenn Greenberg and John Shapiro, Eddie Lampert, Richard Perry and Seth Klarman. The others on the list, including Randy Updyke and Thomas Sweeney, seem to have chosen a quieter path or retired early. The fact that so many of these managers have, in fact, “gone on to investing fame and their clients to fortunes” speaks volumes about the ability of investors to identify great managers.

Finding managers with the requisite ethics, aligned incentives, proper temperament and a disciplined value-oriented approach will go a long way toward ensuring long-term performance success.

Size matters (but not how you think it does)

In addition to the qualitative characteristics above, what other things should investors look for in choosing money managers? In Modern Portfolio Theory IS Harming Your Portfolio, I suggested that smaller firms are often in a better position to manage assets, because they are free from the rigidity of investment committees, corporate culture and the difficulty of quickly deploying assets when an opportunity arises.

The cultural constraints I was referring to were highlighted in Comfort is Rarely Rewarded; Maverick Risk and False Benchmarks, where I argued that too many in our industry have become asset gatherers instead of asset managers, favoring the business of investing at the expense of the profession of investing. When firms become successful and large, it becomes increasingly difficult for them to focus on investment results for their clients.

In a January 2009 paper entitled, “Does Size Matter in the Hedge Fund Industry?”, Melvyn Teo concluded there was a negative, convex relationship between hedge fund size and future risk-adjusted returns.

He examined hedge fund returns from January 1994 through June 2008 using monthly net-of-fee returns from 3,177 live 4,240 shuttered hedge funds allocated to four styles over the period. (Including shuttered funds eliminates survivorship bias.) He found that a portfolio comprised of the smallest 40% of hedge funds outperforms a portfolio of the largest 40% hedge funds (both rebalanced annually) by a risk-adjusted 3.65% per year. Similarly, a recent Wall Street Journal article, “When to Trust a Hedge-Fund Rookie,” found that less tenured managers (those with two years or less of experience) outperformed their more experienced peers with annualized returns of 16.5% versus 10.7%between 1995 and the first quarter of 2011.

The idea that larger managers have a harder time outperforming has been found in a variety of research on mutual funds as well. Several recent studies have taken an even deeper look at what distinguishes investment managers and how those differences impact performance. An analysis by consulting company Kasina — highlighted in its article, How Advisors Select Investments — found that manager tenure has consistently ranked in the top five factors driving manager selection decisions. Yet, when Kasina examined 3,000 mutual funds for the three-year period ending January 1, 2011, they found only a 0.06 correlation between manager tenure and return relative to the fund’s benchmark. Essentially, more experience did not equate to better returns.

In another 2009 paper, “Investing in Talents: Manager Characteristics and Hedge Fund Performances” Li, Zhang and Zhao took a comprehensive look at fund characteristics such as fees, structure and size as well as manager characteristics including age, work experience, tenure with the fund and educational background. While they also found that fund size was negatively correlated to performance, their findings regarding work experience were most notable.

Less experienced managers had superior performance. Their empirical research supports the hypothesis that “the impact of career concern dominates that of working experience,” and that less experienced managers have stronger incentives and more willingness to take risks, often leading to superior performance.

Most people would find this concept somewhat shocking. Consider how many firms espouse the experience of their managers as a key selling trait. The idea that experience might actually be detrimental to returns is not one that the investment management industry is willing to promote. However, an intellectually honest assessment of the role of experience in driving investment decision-making and results is in the best interest of advisors, managers and clients alike.

It is not difficult to understand the power of incentives and their effect on work ethic and career concern, particularly in the lucratively compensated hedge fund world. However, there may be other reasons why experience is not necessarily positively correlated with investment returns.

Young brains: Experience vs. exposure

I recently attended a panel discussion on tail-risk hedging featuring three money managers devoted to that complex and increasingly popular strategy. Aside from the moderator on the panel, the elder statesman of the group was in his late 30s. None of these young bucks had even been in the business during the tail-risk event that gave such occurrences their name – the stock market crash of 1987. Struck by the youth of the panel, I was reminded of Michael Lewis’ observation in Liar’s Poker describing the protagonists of the then-newly developing mortgage bond market. “A young brain leaped at the chance to know something his superiors did not,” Lewis wrote. “The older people were too busy clearing their desktops to stay at the frontiers of innovation.”

In his 2001 shareholder letter, Warren Buffett distinguished between experience and exposure and argued that most investors mistakenly focus on experience when they should focus on exposure. This came from a man who has heaps of both. Relying heavily on experience tends to mean looking to the past and considering the probability of future outcomes based on how things played out historically. Exposure, on the other hand, considers the likelihood — and potential risk — of an event that recent history may not reveal.

Perhaps even more importantly, relying on experience often means relying on a cloudy, biased recollection where our “memory is not as much a factual recording of events as it is a perception of the physical and emotional experience,” as behavioral finance professor John Nofsinger teaches us. Focusing on exposure, on the other hand, frees us to think beyond what our experience allows for. Perhaps ironically, forsaking experience for exposure may allow for a greater respect for the rhythm of history with a more objective and long-term analysis.

The fruits of this labor were driven home in This Time Is Different: Eight Centuries of Financial Folly, by Carmen Reinhart and Ken Rogoff, who documented consistent historical patterns in financial crises and subsequent recessions over a long time frame and across many countries.

In practical terms, most investors today are impaired by their experiences in the 1980s and 1990s. They lack a historical understanding of secular market cycles and valuation, the closest thing we have to a law of gravity in finance. Similarly, most economists, with their data-heavy analysis, lean almost exclusively on the post-war period when modeling how the economy should behave. Most economists, strategists, analysts and investors have not experienced debt-induced financial crises, de-leveraging global economies or the demographic headwinds we face today. Nor does anybody’s experience include the ways in which today’s world is unique from any other point in history and the ways in which tomorrow’s history is completely unwritten.

To avoid the risk of being accused of ageism, I want to be clear that the disposition to rely on what we think we already know is a universally human trait. The challenge is just that older people already know so much more than their younger, less experienced counterparts. As Charlie Munger quipped, “The human mind is a lot like the human egg, and the human egg has a shut-off device. When one sperm gets in, it shuts down so the next one can’t get in.”

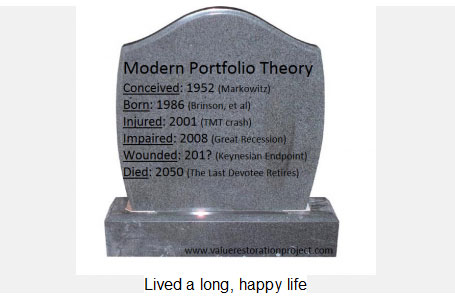

This makes the experienced mind predisposed to missing regime changes and paradigm shifts that define the world in which we live and invest. These paradigm shifts can include anything from changes in the direction of long-term valuations and thus long-term returns to changes in the value of the currency in which we measure everything to changes in the theories that inform our decisions, such as modern portfolio theory.

Perhaps we are witnessing the end of the belief that stimulative government policies will always succeed at growing the economy, as argued by PIMCO’s Tony Crescenzi in the Keynesian Endpoint. As technology increases the pace of regime changes and paradigm shifts, the need to identify managers with the right exposure, rather than experience, is critical.

A recent Farnam Street Blog post asks How to orchestrate a paradigm shift?, and looks to science and The Structure of Scientific Revolutions by Thomas Kuhn for some insight. Kuhn argues that scientific progress is marked by anomalies that fall outside of the conventional wisdom or accepted scientific principles of the day. These anomalies are studied in a wide variety of ways until they become blurred. Eventually, Kuhn notes, practitioners cannot agree on what the paradigm is and “formally standard solutions of solved problems are called into question.”

“A reconstruction of the field from new fundamentals, a reconstruction that changes some of the field’s most elementary theoretical generalizations as well as many of its paradigm methods and applications” ensues, Kuhn writes Almost always, those who manage to identify the shifting paradigms are either young or inexperienced, making them more likely to see that old rules no longer apply and a new set has replaced them.

It is precisely because they lack experience and the baggage of old paradigms that the relatively young or inexperienced are able to see the fundamental shifts underway and change course as necessary. The Farnam Street Blog quotes Max Planck: “A new scientific truth does not triumph by convincing its opponents and making them see the light, but rather because its opponents eventually die, and a new generation grows up that is familiar with it.”

Some truths — like the long-term trends of valuation expansion and contraction or the power of fear and greed to impact asset prices — live and die again with each cycle. Other “truths,” like the efficient market hypothesis and modern portfolio theory, will perhaps go the way of the buggy whip. If Planck’s observation is right, we should be able to pinpoint the approximate date of death to 2050, when the last 25-year old who entered the business in 2000, trained on the “truths” learned in the decades prior, finally decides to retire.

Or perhaps we will not have to wait that long. The highly social and reflexive nature of markets and economies distinguishes investing from the hard sciences. Copernicus proved mathematically that our system was heliocentric — the Earth and other planets revolve around a stationary sun — as opposed to geocentric, a model that places Earth at the center. His models were at odds with not only conventional wisdom but also the then-prevailing understanding of the Bible and teachings of the Church. It took more than 60 years, well after Copernicus and his critics had died, before the observations of Galileo, supported by Copernicus’ early work, were enough to change the views of contemporary astrologists, the Church and the people.

If we are convinced of the idea that success in the markets requires us to evolve, to hold old ideas lightly, to seek anomalies and disconfirming evidence, to dedicate ourselves to lifelong learning and to identify and align ourselves with the many paradigm shifts constantly underway, then there are things we can do to make that process easier. While T. Boone Pickens probably has good genes to thank for having the brain function and physical health of a man half his 83 years, a healthy, active lifestyle and a preference to surround himself with “sharp young minds” rather “than play golf and gin rummy all day” certainly helps Despite being in his 80s, T. Boone is Michael Lewis’ “young brain,” eager to learn something others do not know.

Similarly, playing on the back nine of his career has not prevented Jeremy Grantham from continuing to shepherd his clients’ asset through a variety of paradigm shifts. Lastly, Jim Ware and his Focus Consulting Group have identified that investment managers who meditate, among other things, are more likely to remain curious and open, allowing the “very best thinking – creative and insightful” to take place.

Bringing it all home: What we know and what we don’t

The fact that the “New Warren Buffetts” article from 1989 correctly identified so many successful managers based essentially on their qualities alone is only anecdotal evidence for the philosophical belief that investors can and should seek outstanding managers to shepherd their capital. The fact that smaller managers tend to outperform is supported by empirical evidence alongside the logical argument for why incentives and cultural and organizational factors might make it so. The idea that more experience does not lead to better results also has empirical support, but the logical and philosophical argument is not widely addressed or accepted. This is probably because admitting to a limit of the benefit of experience on investment results is akin to admitting our weaknesses and our vulnerabilities. As Tom Brakke of the Research Puzzle noted,

The investment professional is caught between two realities: Clients want answers and markets are unpredictable. … Zweig reminded me what Peter Bernstein said was the major lesson that he had learned during his long career. Simply, it was that “we don’t know what the future holds.” We forget that first principle all too frequently on our own, and by its nature the investment business encourages that amnesia.

Truly successful managers, advisors and investors will embrace the unknown. They will leave behind the large and traditional for the small and maverick. They will forsake their experience and what they’ve learned in the past in order to gain greater exposure and a better chance to identify what will be important to know in the future.

J.J. Abodeely, CFA, CAIA is a director and portfolio manager at Sitka Pacific Capital Management, an absolute return-oriented separate account asset manager. He writes at www.valuerestorationproject.com.

Read more articles by J.J. Abodeely, CFA, CAIA