Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This essay is excerpted from the most recent version of The Credit Strategist (formerly the HCM Market Letter). To subscribe directly to this publication, please go here. The Credit Strategist is on Twitter - @credstrategist

“The foundation of any liberal society is the willingness of all groups to compromise private ends for public interest. The loss of civitas means either that interests become so polarized, and passions so inflamed, that terrorism and group fighting ensues, and political anomia prevails; or that every public exchange becomes a cynical deal in which the most powerful segments benefit at the expense of the weak.”

Daniel Bell1

As it continues to wrestle with the aftermath of the 2008 financial crisis, America’s policy elites are said to be facing a historic test of leadership. Unfortunately, the way this test is being posed is intellectually flawed and doomed to failure. Democrats and Republicans are arguing over monetary and fiscal policy without adequately addressing the broad legal, regulatory and tax policy regimes that favor debt over equity and speculation over productive investments. The so-called choices being posed are really false choices because they are two versions of the same pro-cyclical ideologies that have trapped the economy in a boom-and-bust cycle. The Obama and Ryan budget plans both leave the United States grossly over-indebted and therefore consigned to years of below-trend growth and financial fragility. Europe is basically following the same path while wrestling with deep structural flaws in its union.

Virtually every public opinion poll tells us that American elites have fallen into profound disrepute. Daniel Bell described an elite as follows: “An elite, at best (as in an Establishment), serves as a source of moral authority and political wisdom.” Speaking of the elite that formed after World War II, he argues that “it was not their interests that defined them as an elite, but their character and judgment. The important consideration was that their opinions had weight because they were respected. Reciprocity between judgment and respect is a necessary condition if policy is to be tempered by the weight of elite opinion.”2 American’s hegemony was always based on moral as well as military and economic strength. While American values have been called into question in the past (for example, during the Vietnam War), there is a sense that the financial crisis broke new ground in sowing doubts about how the U.S. treats the rest of the world as well as its own disenfranchised citizens.

The export of toxic investments to institutions and governments around the world struck an indelible blow against American moral and intellectual leadership. The failure of economic regulators and gatekeepers (such as the credit rating agencies) calls into question the ability of this country to handle the complex intellectual challenges posed by a globalized and interconnected world. Unfortunately, the aftermath of the crisis has done little to dissipate these doubts. Regulatory reform has at best occurred at the margins, and the big issues such as derivatives regulation and “too big to fail” have been left unaddressed. Dodd-Frank appears to be one of the sloppiest, vaguest and most complex (and the contradictions among those adjectives are deliberate) pieces of legislation ever passed by Congress. Fatally, the measures taken to prevent another crisis have been based on flawed ideas such as the Efficient Market Theory and the fantasy that human beings are rational beings when precisely the opposite assumptions are required to forge effective reforms. Until the leaders of the West alter their allegiance to traditional ways of thinking about money and economics, the global economy will stumble.

The U.S. economy

Investment performance for the rest of the year will be determined by the macro-economic views of investment managers. While macro-economic factors are always extremely important in charting investment strategies, they are particularly important today as the U.S. and global economies continue to fight their way through the detritus of the global debt crisis. A compelling case can be made for weaker 2Q112 growth based on a combination of factors that include the following:

- the termination of QEII;

- the Japanese earthquake’s impact on global supply chains;

- higher energy prices;

- slower state and local government spending;

- bad weather; and

- incessant weakness in the housing and jobs markets (which are connected).

Most important, these factors are largely symptoms of policy failures. Even Acts of God are colored by the possibility that man could have better planned for such inevitable but temporally unpredictable events (and this does not even include the possibility – about which we express no opinion here – that global warming played a role).

Accurately identifying the underpinnings of economic growth (or weakness) is particularly important today. If cyclical factors such as energy prices, Japan and even bad weather are the primary drivers of slower growth, investors can justifiably expect the current soft patch to pass relatively quickly. If, however, the structural problems plaguing the U.S. economy (high debt levels, etc.) are retarding growth, the slowdown is likely to be extended. Structural problems are far more likely to lead to a systemic crisis than factors that are likely to fade with the passage of time. As readers familiar with The Credit Strategist would expect, I believe that the problems affecting the economy are structural rather than cyclical. I expect economic growth to remain below trend (until slow growth becomes the trend) unless the current policy regime is altered. I have been called naïve (or worse) for even writing about the possibility of such a policy shift, but I believe that there is no choice but to work toward such change. If we think about how we all felt at the height of the crisis, we can agree that the alternatives are too bleak to accept.

The housing market

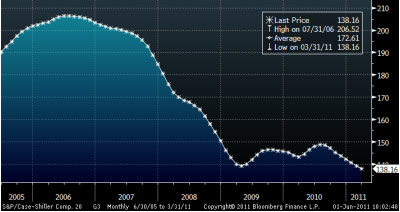

One sector clearly suffering from deep structural and cyclical problems is the housing industry. At this point, the evidence is irrefutable that the housing market is not recovering. The most recent Standard & Poor’s/Case-Shiller National Index showed a 4.2 percent drop in nationwide home prices in 1Q11, which followed a 3.6 percent drop in 4Q10. This was the eighth straight decline and brought prices back to 2002 levels. David Blitzer, chairman of Standard & Poor’s index committee, told The Wall Street Journal (“Housing Imperils Recovery,” June 1, 2011, p. A1) that “[h]ome prices continue on their downward spiral with no end in sight.” The most recent report signals “a double dip in home prices across much of the nation.” As Figure 1 below illustrates, rather than a double dip, it is probably more accurate to say that the housing sector never recovered at all but was simply temporarily boosted by government tax credits.

The Credit Strategist thinks it should be a point of particular concern that the Federal Reserve’s sustained zero interest rate policy was unable to stimulate housing. This failure is evidence that what ails housing is structural rather than cyclical, and it will require structural rather than merely cyclical policy changes to fix it. There is still far too much excess housing stock as a result of policies that promoted home ownership to an extent that transformed housing into a financial asset rather than as a utilitarian asset that is primarily designed to provide shelter to its owner. It is time to acknowledge that housing is not a particularly productive asset that has been subsidized far beyond its contribution to economic growth. The fact that there are still hundreds of thousands of housing starts each month truly beggars reason.

Figure 1

Case-Shiller 20 City Index

Home prices are now 35-40 percent below their 2006 peak, but there is no God-given reason why they can’t drop further. If home prices are continuing to decline while the economy is enjoying record low interest rates, it would appear that there is something other than affordability suppressing prices. According to The Wall Street Journal, median earners today can afford 75 percent of all homes sold.3 Among the factors that are likely pushing down prices is the tepid job market, millions of empty and foreclosed homes, and buyers’ beliefs (or fears) that prices are going to continue to decline. While all of these factors should raise concern, the last one –deflationary psychology – may be the most dangerous. If such psychology were to gain momentum (if it hasn’t already done so), it could drive prices considerably lower. After all, isn’t it reasonable to believe that most people who want and can afford a home already own one? And if that is the case, how many people are going to run out to buy second homes? One of the big negative surprises that may haunt the markets and the economy for years to come is not simply that house prices aren’t going to recover quickly but that they may also drop significantly further from their peak. While the Obama Administration has tried virtually every traditional remedy to prop up housing, none of them have worked. It is time to change the underlying policies that created this mess in the first place.

1. Daniel Bell, The Cultural Contradictions of Capitalism (New York: Basic Books, 1978), p. 245.

2. Bell, p. 201.

3. The Wall Street Journal, June 2, 2011, “The Housing Illusion,” p. A18. I strongly recommend this editorial to my readers.

Capital spending

Capital spending by corporations has been one of the strongest drivers of whatever economic recovery the U.S. has enjoyed since the financial crisis. These expenditures dried up during the financial crisis, causing healthy companies to increase their post-crisis spending in order to catch up and maintain their capital stock. Slower capital expenditures constituted much of the drop in GDP during the crisis and much of the recovery in GDP thereafter. Now that most of the catch-up capital spending has run its course, capital expenditures are likely to track or even lag economic growth. The reason for this is that many sectors of the economy remain plagued by overcapacity. Current capacity utilization remains below trend at about 80 percent. In past cycles, capital spending began to fade only when private sector demand had recovered from the previous downturn. That is not the case today, as private sector growth remains tepid and households are still struggling. If monetary and fiscal tightening arrives over the second half of 2011, strong capital spending is unlikely to make up the shortfall in growth. Slower capital spending gives the Federal Reserve one more reason to delay raising interest rates until well into 2012.

Weaker capital spending may have contributed to the horrible ISM number released on June 1. While a weak number was expected due to supply chain disruptions caused by the Japanese earthquake and tsunami, the ISM factory index for May came in at a lower than expected 53.5, down from 60.4 in April and the lowest level since September 2009. This suggests that companies are slowing capital spending beyond what can be accounted for by a manufacturing slowdown triggered by a lack of part supplies from Japan.4

QEIII?

QEII accomplished little (other than perhaps convincing investors that its termination would lead the economy to slow down). QEIII would do little more than increase the federal debt and demonstrate that the Federal Reserve learned nothing from its earlier mistakes. Little of the funds injected into the banking system found their way into new loans, and $600 billion was too small to make much of a difference in a $14 trillion economy anyway (whatever economists will tell you). Instead, the Federal Reserve’s post-crisis policies have indiscriminately sprayed the economy with liquidity, most of which found its way onto the balance sheets of large banks who do not want to admit that many of their assets (i.e. mortgage securities, private equity holdings) are not worth their book value and need to run a massive carry trade with these funds to eat up losses. Rather than low interest rates and more liquidity, the economy needs policies that will direct the already excessive liquidity in the system toward productive uses such as education and scientific research and development, as well as into industries such as energy and healthcare. The last thing this economy needs is further injections of cheap liquidity into the already overleveraged financial sector. The types of policy changes needed would create incentives for economic actors to invest in productive activities, and the main tool whereby these changes would be implemented is the tax code. The incentives currently built into the tax code (and further supported by regulatory policy) favor debt over equity and speculation over productive investment. Until these incentives are reversed, there is little hope that the U.S. economy will be able to reverse its current self-destructive course.

Balance sheet recession?

The Credit Strategist has written extensively on the efforts U.S. companies made to reduce their debt in the immediate aftermath of the 2008 financial crisis. While these moves were eminently sensible for the individual companies themselves, they collectively resulted in an economic slowdown and deflation. This phenomenon has been called a “balance sheet recession” by Richard Koo, who has written two excellent books on the subject.5 He writes, “[a]lthough repaying loans is the correct (and responsible) course of action for individual firms, when pursued by all firms at once it leads to a disastrous fallacy of composition. This is the most frightening aspect of what may be called a balance sheet recession, in which firms are no longer maximizing profits, but are minimizing debt instead.”6 Too many companies paying down debt at the same time slows economic growth. Koo’s policy solution for a balance sheet recession calls for the central bank of a country experiencing such a recession to borrow to compensate for private sector savings. Thus far the Federal Reserve has followed this script. The problem is that the money the Federal Reserve has been borrowing has ended up nesting on bank balance sheets rather than circulating in the economy producing jobs and growth. The money multiplier has not worked as advertised (another sign of the infirmity of traditional economic thinking). Healthy corporations that cut debt during the crisis and then increased this spending in order to catch up are now slowing this spending again. The jobs market is slowly improving, but this is apparently due to the fact that fewer workers are being fired as part of corporate austerity measures rather than massive doses of new hiring. All indications are that something like a balance sheet recession is occurring in the United States. If this proves to be the case, the economy is not experiencing a self-sustaining recovery but may instead be doomed to years of sluggish growth (like Japan).7

Mr. Koo also makes the bold claim that the money being saved by U.S. corporations will be available for borrowing by the U.S. Treasury. In a 2009 interview with Kate Welling, he said that “once a country enters a balance sheet recession because the private sector is paying down debts, you end up having excess savings in the private sector and it is those excess savings that the government has to borrow and spend. It doesn’t have to borrow externally.” (welling@weeden, Vol. 11, Issue 17, September 11, 2009, “Koo’s ‘Good News’”).8 Based on this scenario, the Federal Reserve can continue to borrow from the banks, which are hoarding most of this money, and the more it borrows the more the banks will buy. In fact, as noted in last month’s issue of this publication, banks are seriously underweighted Treasuries and have the potential to purchase considerably more of them. This is all well and good, but unless the money ultimately finds its way into productive uses in the economy, it will most likely be used for speculation by these banks (despite the so-called Volcker Rule) and their hedge fund and private equity clients. This will still leave the U.S. with below-trend growth as the federal debt burden continues to swell.

The European debt crisis

European leaders appear to be hell-bent on repeating their past mistakes and bailing out Greece a second time. Luxembourg’s Jean-Claude Juncker, speaking for the collective finance ministers of the European Union, stated on May 30 that a complete restructuring of Greece’s debt is not in the cards. The European Central Bank (ECB) appears unalterably opposed to default due to fears about the European banking system. Pain deferred, however, is pain increased, and avoiding a painful default today will only cause a more painful default in the future. What needs to happen today is a complete restructuring of Greece’s debt that would inflict losses on bondholders rather than another bailout that places those losses on the backs of taxpayers.

Any course of action other than a default is delusional. The financial markets are now closed to Athens. Greece’s 10-year bonds are yielding almost 17 percent. Its two-year paper trades at 25 percent, creating an inverted yield curve signaling the market’s judgment that Greece cannot meet its obligations. (By way of comparison, among future default candidates, Spain’s two-year debt still trades at a far too low 3.52 percent, while Portugal’s and Ireland’s two-year paper trades at more realistic – but probably too low – yields of 10.9 percent and 11.8 percent, respectively.) At the time of Greece’s original bailout a year ago, it was thought that Athens would need at least €30 billion to tide it over to next year, when it was expected to be able to return to the markets to raise capital. Now it is clear that Greece’s access to the markets is closed.

Figure 2

The Market Sends Greece to Hell

Despite the obvious need to allow Greece to default, there still appears to be insufficient political will to institute such an action. But until Greece defaults, the ECB and other institutions dumb enough to sink more money into a hopelessly bankrupt company will simply be perpetuating the flawed policy regime that led to the current crisis. Capitalism for the rich and socialism for the poor doesn’t serve the rich or the poor particularly well (even if the rich are congratulating themselves on their supposed brilliance). Bailing out Greece will do nothing for disenfranchised European taxpayers while providing one more escape route for large institutions and other powerful economic and political interests. It is not merely an economic policy error because it treats the symptoms but not the disease, but is a profound moral error as well. Now is the time for Greece to default and inflict on its bondholders – who were imprudent enough to buy its debt in the first place – the losses they deserve.

The latest reports out of Europe are that Greece will agree to further austerity measures in exchange for the IMF releasing the next €12 billion tranche of aid under the original bailout plan. Earlier reports suggested that the ECB and IMF were asking for control of Athens’ pathetic tax collection and privatization efforts in exchange for further aid. This would effectively constitute Greece handing over its sovereignty to the European Union and IMF, a politically impossible choice for Greece’s leaders. But the fact that such a radical approach is being proposed suggests the depth of Greece’s failure to reform its internal finances. It is increasingly clear that the rest of Europe doubts Greece’s ability to put its own financial house in order. Germany is resisting another bailout as Chancellor Angela Merkel comes under increasing political pressure to abandon that country’s Southern neighbors. Yet it appears increasingly likely that Germany will not stand in the way of a second bailout. Perhaps Frau Merkel took a hard look at German banks’ exposure not only to Greece but also Ireland and Portugal and decided that kicking the can down the road for the next Chancellor is the better form of valor. This may hasten her status as a former Chancellor, but more significantly signals the abdication of the strongest European voice in favor of fiscal discipline.

4. Among the steps being taken by Japan to get suppliers back on their feet is a relatively modest $620 million fund being set up by the Development Bank of Japan to provide capital to those auto-parts makers hit by the earthquake and tsunami.

5. Richard C. Koo, Balance Sheet Recession: Japan’s Struggle with Uncharted Economics and its Global Implications (Hoboken: John Wiley & Sons, 2003) and Richard C. Koo, The Holy Grail of Economics: Lessons From Japan’s Great Recession (Hoboken: John Wiley & Sons, 2008).

6. Koo, 2008, p. 19.

7. The May jobs report supports the thesis that the U.S. is experiencing some type of balance sheet recession. The 0.3 percent increase in hourly wages coupled with weak job growth suggests that companies are acting cautiously and stretching their existing staffs rather than making new hires. This is rational behavior for the individual companies but when this behavior is aggregated across the economy it results in slow growth.

8. This argument provides an interesting perspective on Kyle Bass’s argument that Japan is on the verge of exhausting its domestic savings and will be forced to raise funds externally, which would lead to higher interest rates. Mr. Koo appears to dismiss Mr. Bass’s view and argue that domestic funds will remain available for borrowing as long as Japan remains in a balance sheet recession. Mr. Koo appears to be describing accurately what happened in Japan in the past while Mr. Bass is suggesting that Japan cannot continue indefinitely to depend on internal funds once it reaches its Keynesian Endpoint.

The most important question for investors is whether a Greek default will spread to the rest of Europe and then to the United States. European banks hold billions of dollars of Greek debt and will suffer painful losses in the event of a default, although nobody seems to know at what value these banks are carrying their Greek debt. If contagion occurs, it will result from the web of credit default swaps that connects European banks and the U.S. financial institutions that were willing to stand on the other side of their Greek trades. Of course, there is no way to know precisely how much CDS has been written on Greek sovereign debt because the credit derivatives market remains – more than two years after the derivatives-driven financial crisis of 2008 –unregulated and opaque.9 Accordingly, contagion fears may be justified but are impossible to gauge accurately until a default occurs.

Whatever scenario unwinds, Europe’s banks are facing serious challenges. According to Dealogic, European banks must refinance €1.3 trillion of debt through the end of 2012. If refinancing becomes difficult for Europe’s banks, that will not be good for the U.S. banks that are counterparties on trillions of dollars of credit default swaps on Greek debt and virtually everything else under the sun. (As it is, U.S. bank stocks are crawling over each other to earn the title of “new dogs of the Dow.”) The gargantuan refinancing needs of Europe’s banks weigh strongly against further interest rate increased by the ECB, which may be consigned to using its bully pulpit alone to fight the ghosts of Weimar. The last thing Europe’s banks need as they try to climb their massive refinancing wall is higher interest rates. What the global economy needs is counter-cyclical monetary policy (higher rates and tighter liquidity) to start down the road to financial stability.

The view that monetary policy needs to tighten diverges from the views of some of Wall Street’s best minds. For example, the well-respected (including by us) Michael Darda of MKM Partners warned in week’s Barron’s (May 30, 2011, pp. 5-6) of the dangerous consequences of the ECB raising interest rates. He notes what The Credit Strategist has been arguing for many months, that the bailout/austerity policy mix has failed. He also suggests that the ECB should take further steps to loosen monetary policy in order to avoid deflation. Deflation would cause higher unemployment, weak GDP and lower tax revenues, exactly the conditions plaguing the weaker European nations today. The problem with this argument is that it does not offer a way out for these countries. There is no painless way out of the current economic mess into which a pro-cyclical monetary regime has pushed Europe. It is time for the European elite to educate European voters that continuing the same failed policies of the past is only going to harm Europe’s economic future. That is what elites are supposed to do – educate and lead, not cynically manipulate the system for their own gain.

Assuming the wrong policy choices will continue to be made and Greece’s default will be delayed, the question remains how long the ECB can delay the ultimate day of reckoning for Europe and particularly for its weaker Southern countries? In view of the Brobdingnagian amounts of money that the ECB and Federal Reserve have printed, it is also fair to ask whether any of the remaining tools in their arsenals can prevent runaway inflation on the other side of the current slowdown?

Investment recommendations

The global economy is extremely fragile today. Markets have not fully recovered from the financial crisis and have failed to adopt the necessary reforms to strengthen the system and right the wrongs of the past. Accordingly, the system remains highly vulnerable to further disruptions. That means volatility should rise, interest rates should go lower, the euro and dollar will continue to weaken against Asian currencies and gold, and the equity market (as well as its dark twin, the high yield bond market) should be approached with a great deal of caution. Our specific investment recommendations this month are as follows:

-

Gold. We continue to recommend that gold should constitute 10-15 percent of any portfolio. As long as central bankers and politicians control money, fiat currencies will continue to deteriorate in value against gold. We recommend purchasing physical gold, but the gold ETF (GLD) or the Sprott Physical Gold Trust (PHYS) are decent alternatives as well.

-

Fixed Income. At the current time, we recommend a minimal fixed income allocation despite the fact that we expect rates to go lower due to economic weakness and structural/political factors that favor low interest rates. High yield bonds are priced at their lowest yields in history and offer an extremely poor risk/return profile. While there will likely be a limited number of defaults in the near future, defaults will occur sooner or later (sooner if the economy remains weak, which is our expectation), and single digit yields are simply insufficient to compensate for the risk of owning hybrid debt/equity securities. It is too early to short Treasury bonds, but sooner or later they may well end up being what our friend Doug Kass has termed “the trade of the decade.”

-

Bank Debt. Bank debt remains the safest way for an investor to obtain a decent yield on his or her money. We continue to recommend two stocks as the best way to gain access to the institutional bank loan market – Kohlberg Kravis Financial Products (KFN) and Tetragon Financial Group Limited (TFG1). KFN trades near book value and pays better than a 6 percent dividend. TFG trades at a 25-30 percent discount to book value and pays a 4-5 percent dividend. TFG was recently added to the MSCI Small Cap Index and appears to be attracting the attention of value-oriented hedge funds.

-

Stocks. The stock market is subject to significant macro-economic risks today and must be approached with caution. Value-oriented strategies focused on reasonably large cap stocks and special situations should be the best performers in such an environment. We continue to recommend British Petroleum plc (BP) and also suggest investors avoid bank stocks for now. Among other problems, banks are facing tens of billions of dollars of potential liability related to the financial crisis that the market should be taking more seriously than it is. Bank stocks should remain under pressure for the foreseeable future despite the record low interest rates they are enjoying, which suggests just how badly impaired they were by the crisis.

-

Currencies. We continue to expect the dollar and Euro to continue to weaken against Asian currencies, the Swiss franc and gold. We have changed our view about the Euro/dollar trade and believe that the Euro could continue to weaken against the dollar in the near-term based on the ill-advised approach being taken by the ECB to Greece. There is no end in sight to European bailouts or, put another way, European bailouts will end only when Germany balks at bailing out Portugal and Ireland for the second time or Spain for the first time, an event that will trigger a Euro crisis that would lead the Euro to drop in value against even Zimbabwe’s currency.

-

Volatility. We have believed for a long time that volatility is underpriced. Markets are far too complacent in view of the fragility of the global financial system. The best way to play volatility is through options on the VIX. Volatility ETFs are, like many macro-oriented ETFs, flawed in design and will not give investors the bang for the buck they can obtain through options.

Based on our reading of monetary and fiscal policy and other macro-economic trends, The Credit Strategist assumes that the markets will continue to be stuck in the boom-and-bust cycle of the last thirty years. As a practical matter, this means that the most important thing an investor can do is protect against the large losses that occur with the downside of this cycle. Investors learned the hard way in 1994, 1998, 2001-2 and 2008 that it’s not what you make, it’s what you keep. Unfortunately, investors tend to act in a pro-cyclical manner by which they earn good returns when the market goes up and gives all of those returns back (and more) when the market corrects. This behavior is one reason why so many institutions are experiencing significant funding deficits – their obligations continue to grow while their investment returns fail to keep up due to the large losses they suffer in down years. My approach (and advice) is for investors to act in a counter-cyclical manner that still allows them to profit in good markets but also allows them to avoid large losses in bad markets.

Michael E. Lewitt

June 3, 2011

9. According to the Bank of International Settlements, the notional amount of outstanding over-the-counter derivatives stood at $601 trillion in December 2010 compared with $603 trillion at the end of 2009 and $684 trillion in December 2008. Interest rate contracts accounted for $465 trillion of the December 2010 total, which is higher than their pre-crisis level. The BIS suggests that gross market values, which represent the cost of replacing all existing contracts, more accurately reflects the at-risk amounts. The gross market value was $24.5 trillion at the end of 2010 – a mere bagatelle!

Disclosure appendix

This publication does not provide individually tailored investment advice. It has been prepared without regard to the circumstances and objectives of those who receive it. This report contains general information only, does not take account of the specific circumstances of any recipient, and should not be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. Each recipient should consider the appropriateness of any investment decision having regard to his or her own circumstances, the full range of information available and appropriate professional advice. The editor recommends that recipients independently evaluate particular investments and strategies, and encourages them to seek a financial adviser’s advice. Under no circumstances should this publication be construed as a solicitation to buy or sell any security or to participate in any trading or investment strategy, nor should this publication or any part of it form the basis of, or be relied on in connection with, any contract or commitment whatsoever. The value of and income from investments may vary because of changes in interest rates or foreign exchange rates, securities prices or market indexes, operational or financial conditions of companies, geopolitical or other factors. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. The information and opinions in this report constitute judgment as of the date of this report, have been compiled and arrived at from sources believed to be reliable and in good faith (but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness) and are subject to change without notice. The editor may have an interest in the companies or securities mentioned herein. The editor does not accept any liability whatsoever for any loss or damage arising from any use of this report or its contents. All data and information and opinions expressed herein are subject to change without notice.

The Credit Strategist

Michael E. Lewitt, Editor

The Credit Strategist is published on a monthly basis by Michael E. Lewitt. Address: 5030 Champion Blvd., G6 #161 Boca Raton, FL 33496. Telephone: (561) 239-1510. Email: [email protected]. Delivery is by electronic mail. Annual subscription rate is $395 for individuals and $995 for institutions. Visit our web site at www.thecreditstrategist.com. Copyright warning and notice: It is a violation of federal copyright law to reproduce or distribute all or part of this publication to anyone (with the exception of individuals within the same institution pursuant to the subscription agreement) by any means, including but not limited to photocopying, printing, faxing, scanning, e-mailing, and Web site posting without first seeking the permission of the editor. The Copyright Act imposes liability of up to $150,000 per issue for infringement. Information concerning possible copyright infringement will be gratefully received.

Read more articles by Michael Lewitt