Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This essay is excerpted from the most recent version of the HCM Market Letter. To subscribe directly to this publication, please go here.

“For it must be cried out, at a time when some have the audacity to neo-evangelize in the name of the ideal of a liberal democracy that has finally realized itself as the ideal of human history: never have violence, inequality, exclusion, famine, and thus economic oppression affected as many human beings in the history of earth and humanity. Instead of singing the advent of the ideal of liberal democracy and of the capitalist market in the euphoria of the end of history, instead of celebrating the ‘end of ideologies’ and the end of the great emancipator discourses, let us never neglect this obvious macroscopic fact, made up of innumerable singular sites of suffering: no degree of progress allows one to ignore that never before, in absolute figures, never have so many men, women and children been subjugated, starved, or exterminated on the earth.”

Jacques Derrida (1993)1

While the late French philosopher Jacques Derrida wrote these words almost two decades ago, they still describe the state of much of the world. After all, it was barely a year ago that Haiti was virtually destroyed by a catastrophic earthquake, and that cursed island remains in the throes of a cholera epidemic and terminal poverty and political chaos. So while much of the financial world is trying to celebrate the start of a new year with optimism, HCM would like to keep things in perspective. The world remains a deeply troubled place, and the amount of intellectual and financial capital that is devoted to money-spinning rather than to productive investment and improving the lives of others is a continuing tragedy.

The consensus has reached the conclusion that financial markets will enjoy a strong start to 2011. This is reason enough to approach the markets with caution as the year begins. When everybody is leaning to one side of the boat, the vessel is far more likely to tip over, particularly if it hits an unexpected wave. The VIX is back down to just a hair above 17, a level that raises warning flags (we always pay special attention when the VIX trades below 20). The complacency to which that VIX level speaks seems misplaced despite the fact that the investing environment has clearly been improving from a lousy base. There are other signs of overexuberance as well, such as the AAII investor sentiment poll hovering above its historical norm for 17 straight weeks, margin debt rising by 16 percent since July to its highest level since July 2008, ETFs attracting gobs of new money, commodity prices going haywire, and the media cheering on the party like it’s 1999. While HCM would certainly take the view that the glass is half full, it isn’t three/quarters full. The balance of positives and negatives is extremely balanced, which means it is a stock picker’s and bond picker’s market.

Interest rates have risen, which HCM considers a good thing since abnormally low rates are always a sign of economic infirmity (as well as policy confusion). It appears that, at least until the next financial crisis, the direction of global interest rates is decidedly upward, despite the Federal Reserve’s obvious goal of negative real interest rates (Federal Reserve Vice Chairman Janet Yellin was quoted as saying during the financial crisis that “[i]f it were possible to take interest rates into negative territory I would be voting for that.”2) The question is whether rates have moved sufficiently higher to negatively impact other markets, particularly the equity and commodity markets. Thus far, the answer is a definitive “no.” Global interest rates are still very low on a historical basis, and certainly not low enough on an absolute basis to retard economic growth or, more importantly (and more destructively in the long run) speculation.3 The issue remains whether the animal spirits of entrepreneurs and investors are awakening, and there are increasing signs that they are.

At the end of the day, however, the economic infirmities of overspending and overborrowing still ail the economy and no painless cures have been discovered. We are very sympathetic with something that Marc Faber wrote in the December issue of his fabulous The Gloom, Boom & Doom Report: “I don’t think that Mr. Bernanke and other central bankers around the world have any intention of ever implementing an ‘exit strategy.’ Maybe on paper the intention is there. Maybe the intention also exists in overstaffed office buildings – full of academics who have never worked a single day in the real economy. However, the reality is that central bankers around the world will continue to pursue expansionary monetary policies. Therefore, I don’t believe that the S&P 500 and other stock markets will retest the March 2009 low.” Based on our agreement with this statement, we continue to recommend that investors continue to accumulate physical gold equivalent to up to 10-15 percent of their portfolios. If history has taught us (and is continuing to teach us) anything, it is that central banks and governments will continue to trash fiat currencies until the end of time. That said, while we think that most of the systemic problems have not been addressed but have largely been pushed off to the future, we also agree with Dr. Faber that the S&P is unlikely to revisit the satanic 666 level in the foreseeable future.

Wall Street strategists were falling over each other to raise their economic growth estimates as 2010 drew to a close. Consensus 2011 GDP estimates are now in the 3.5-4.0 percent range, a sharp increase from the 2-2.5 percent range that dominated discussion earlier in 2010. The revised estimates are likely correct, but like many statistics they fail to tell the entire story. Such growth will only be achieved with a fiscal 2011deficit of approximately 9.5 percent of GDP, which follows deficits of 8.9 percent of GDP in fiscal 2010 and 10 percent of GDP in fiscal 2010. It is safe to say that 2011 GDP growth would be nowhere near 3.5 percent if the U.S. government were not running its budget on steroids. As a new Congress gathers in Washington D.C. with the alleged goal of undoing the fiscal damage of previous Congresses, spending discipline is priority number one. Of course, the lame duck Congress was able to get in its last licks with a tax bill that included payroll and income tax provisions that needlessly benefitted the wealthiest Americans, so the fiscal hole is that much deeper than it needed to be. The Republican-led House of Representatives will have a chance to put its money where its mouth is, so to speak, by proposing meaningful spending cuts, while Democrats try to absorb the lessons of the November 2010 mid-term elections. The most important economic question, however, is whether the private sector will be able to pick up the mantle of economic growth from the government as 2011 progresses and governments at the federal and state levels reduce their spending.

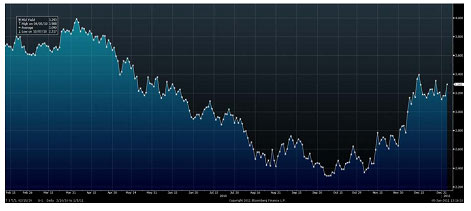

Government bond markets are suggesting that the handoff will not be so easy. When President Obama announced his tax surrender on December 6, the 10-year Treasury bill yielded 2.92 percent, sharply higher than its October low of 2.38 percent. HCM never entertained any serious doubts that the President would cave on the tax issue, which was one of the reasons we started to think that Treasuries were a short when they moved under 2.5 percent. The benchmark bond ended the year at 3.3 percent, and most forecasts see it moving to the 3.75 to 4.0 percent range by the end of 2011.

Graph 1

U.S. 10-Year Treasury Yields – 2010

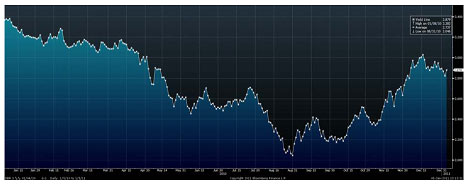

The German bund bottomed at 2.12 percent at the end of August and ended the year yielding 2.93 percent. Hopes (or fears) that its yield would drop below 2 percent were dashed by another outbreak of European credit-sclerosis, this time in Ireland and now threatening to spread to Portugal (whose first bond sale of 2011 came at 3.686 percent compared to 2.045 percent last September), Spain, Belgium and who knows where else.

Graph 2

German 10-Year Bund Yields – 2010

1. Jacques Derrida, Specters of Marx (New York: Routledge, 1994), p. 106.

2. For some reason, this statement reminds us of Cecil Rhodes boast that “I would annex the planets if I could.” This is not a non sequitor if you really think about it.

3. Our friend David Rosenberg points out that banks are engaging in massive proprietary trading activities again. According to Mr. Rosenberg, banks trading assets surged by $64 billion in the last month. See David A. Rosenberg, Gluskin Sheff, Breakfast with Dave, January 4, 2011, pp. 11-12. Perhaps they are trying to get in their last licks before the Volcker Rule takes effect.

As Christopher Wood points out, China is also in a tightening cycle, although in China’s case this is being led by the government rather than the markets, as befits a command economy. China is also raising its interest rates, although it is frankly difficult to determine the precise effect of such moves in a command economy holding more than $2 trillion of reserves. On Christmas Day, China raised its benchmark one-year lending rate and one-year deposit rate by 25 basis points to 5.81 percent and 2.75 percent respectively. Nonetheless, the rediscount rate of 2.25 percent and the one-year relending rate of 3.85 percent remain far below China’s growth rate.

Graph 3

A Command Economy Tightens

The two elephants in the room

Housing

The first elephant in the room for the United States economy remains the housing market, which if it is not at risk of a genuine double dip is certainly not showing signs of a robust or imminent recovery. The October Case-Shiller US Home Price Index was deeply disappointing, with the 10-City and 20-City Composite home prices indices falling by 1.2 percent and 1.3 percent month-over-month respectively on a non-seasonally adjusted basis. On a seasonally-adjusted basis, the indices fell for the fourth consecutive month, with the 10-city index falling 0.9 percent and the 20-city index falling 1.0 percent month-over-month. Year-over-year (October 2010 versus October 2009), the 10-city index is down 0.8 percent while the 20-city index is up only 0.2 percent. This is not the stuff that recoveries are made of.

Graph 4

The Elephant in the Room

Jobs

The other elephant in the room is employment, which is showing minimal signs of life.

The final employment report of the year had a promising headline number of “only” 388,000 new jobless claims, the first print with less than a “4-handle” in a long, long time. Of course, the numbers were dressed-up by a variety of statistical adjustments; the actual non-seasonally adjusted number was apparently 522,000 new claims. More promising, hopefully, was the ADP report on January 5 showing that employers added more jobs in December than at any time since records began in 2001. Employment increased by 297,000 jobs in December after a revised 92,000 rise in November. One can only hope that this trend will continue.

One would hope that the payroll tax reduction that was included in the tax bill passed by the lame duck Congress and signed into law by President Obama in December will encourage companies, which are flush with cash, to begin hiring new employees in the new year. As ISI Group keeps pointing out, however, much of this corporate cash is trapped abroad by punitive U.S. tax laws and is unlikely to wash ashore and be used to hire new workers under the current punitive U.S. tax regime. Furthermore, the ill-advised, badly structured and largely impenetrable healthcare bill that became law last year also discourages new hiring. Symbolic efforts to repeal this law will do little more than stoke partisan fires when what is really needed is an honest discussion about amending the bill to remove its anti-business provisions. The likely course of action will be Republican-led efforts to starve the bill of funding at the state level, which will still leave businesses fearing higher healthcare costs and moving only very slowly to add to their employee rolls. Government giveth with one hand and taketh away with the other. All the while, millions of people suffer without gaining the healthcare that the new law promised or the new jobs that the new law is making it harder for them to obtain.

HCM believes that the housing market will not recover until the jobs markets shows sustainable improvement. This speaks to the fact that policy should have always been focused on jobs rather than gimmicks aimed at the housing market. Trying to keep people in houses they cannot afford is a Sisyphean task. It would be much more promising to create an economic environment in which wages and employment can grow so that more people can afford the houses they live in or want to buy.

Rising oil prices

Readers may be familiar with the story about the frog that is put into a pot of water that is slowly heated up until the water is boiling and the frog dies before he realizes what is happening. The frog doesn’t notice that the water is getting dangerously hot until it is too late. This tale may be an apt description of the apparent indifference to rising oil prices that is being shown by American consumers and businesses. At some point, however, the frog is going to scream (before it expires) if prices at the pump keep increasing.

Some traders and other observers question whether fundamentals support predictions of a $100/barrel oil price. These doubters point to significant excess refining capacity and still sluggish global economic growth. Nonetheless, speculators appear hell-bent on driving the price above $100/barrel during the early part of 2011 (this is confirmed by the near record net speculative long positions in the New York Mercantile Exchange). The value of the dollar will also have a lot to say about where oil trades over the coming months.

Graph 5

The Boiling Frog Syndrome

Long term, of course, demand in places like China and India will continue to rise from extremely low levels and lead to sustained higher prices in the future. For example, Morgan Stanley reported that oil demand increased year-over-year by 9.8 percent in India and 6.5 percent in China. To place this in perspective, world oil demand for the same period increased by only 1.7 percent and dropped by 0.3 percent in North America and was flat in OECD Europe. For the first time in the history of capitalism, according to Dr. Marc Faber, oil consumption growth is higher in emerging economies than in developed economies.4 This is hardly surprising, but it is clear that demand is rising in emerging countries faster than it is falling in developed countries.

Coupled with the apparent decline in currently producing fields and the lag in production, prices are likely headed higher in the years ahead. This renders the stocks of many oil companies attractive. HCM in particular likes British Petroleum plc (BP), Exxon Mobil Corp. (XOM) and Chevron Corp. (CVX). For investors with a high tolerance for risk (and the patience to pour through complicated financial statements) and a desire for exposure to natural gas, HCM also likes Chesapeake Energy Corp. (CHK). Natural gas has been a chronic underperformer in recent years but will benefit if energy prices continue to rise. Carl Icahn recently increased his position in Chesapeake, which HCM recommended last month (before Mr. Icahn’s announcement).

4. Dr. Marc Faber, The Gloom, Boom and Doom Report, January 1, 2011, p. 11.

The new world of technology investing

There appears to be growing excitement about technology among investors. The wireless internet and tablets have clearly captured the imagination of both the media and the public at large, feeding a growing investment frenzy in public stocks like Apple Inc. (AAPL) and private companies like Facebook, Groupon, Inc., Zynga Inc. and Twitter, Inc. Like previous technology bursts, the media-centric nature of technology is feeding into the frenzy. In the late 1990s, the medium for this enthusiasm was the Internet; today it is social networking.

Today, trading in the shares of unlisted companies on exchanges such as SecondMarket is taking off, rendering it unnecessary for companies to go public in order to provide liquidity to their employees. The $450 million investment by Goldman Sachs in Facebook at a $50 billion valuation that was announced on January 3, 2011 stirred just as much excitement in Goldman’s stock as in Facebook’s prospects. Earlier, Twitter announced that it had raised $200 million in a financing that valued it at $3.7 billion and Groupon announced that it planned to privately raise $900 million of additional capital.

The manner in which capital is being accessed raises important policy questions and illustrates important trends in American society. Ben Horowitz, a partner at the venture capital firm Andreessen Horowitz, was quoted in The Wall Street Journal on January 4 as saying that for technology firms, “the incentive for going public has lowered and the penalty for going public has increased…Compared with the 1990s when everybody went public as soon as possible at much lower revenues,” he continues, the regulatory environment and increasing role of hedge funds has made it “dangerous” for technology start-ups to go public without a large cash cushion, which they can obtain through the private market. This is all fine and good except for the fact that these private financings are only available to a small, elite group of investors rather than to the public at large. In addition to its own investment, Goldman Sachs obtained the right to distribute an additional $1.5 billion of Facebook stock to its clients. One can be sure these shares

will not be sold to Ma and Pa Kettle. This is precisely the opposite of the route to public ownership taken by Google, Inc., which engaged in a public auction of its shares.

At the very least, it is ironic to see technologies that are designed to empower consumers and the masses seek financing in a manner that basically disenfranchises them. This is simply another symptom of a system that serves a small elite at the expense of society as a whole. Mark Zuckerberg supposedly wanted to change the world by founding Facebook. He did change the world (not for the better as far as HCM is concerned, but that is a discussion for another day), but his financing maneuvers are simply perpetuating the inequitable financial system that lies at the heart of so many of the ills in our modern world. The insiders who are able to buy these shares have taken risk, but they will also be the greatest beneficiaries of the future success of these companies. The hoi polloi will not even be given an opportunity to take that risk.

Recommendation changes

We would like to amend two of our recent investment recommendations (taking advantage of John Maynard Keynes’ adage that we reserve the right to change our minds when the facts change – or our own adage that we reserve the right to change our minds when we change our minds!).

First, despite the fact that we continue to believe that General Motors (GM) had no business going public with a qualified accounting opinion, the near-term direction of the stock is decidedly upward. Therefore, investors should not be shorting GM, which is turning out to be a play on a U.S. economic recovery that is unlikely to disappoint in the near future.

Second, several months ago we recommended that investors short Yahoo! Inc. (YHOO) after another outburst by its potty-mouthed CEO Carol Bartz. The stock reached a 2010 high of $19.00/share in mid-April before falling to slightly above $13.00/share at the end of August but has since recovered to above $16.50/share. While Yahoo! Inc.’s domestic business appears to be in terminal decline, the company’s holding in Alibaba.com is worth a fortune (and its value is rising) and could be the trigger for a bid from a larger technology company. Our friend Doug Kass is recommending Yahoo stock based on his belief that someone (Doug’s choice is Microsoft, which certainly needs to do something to get people excited about its stock once again) will come along and buy Yahoo! Inc. at a premium to its current price, and he has convinced us that shorting this stock will prove to be a serious mistake.

A contrarian take on Wikileaks

HCM’s first reaction to the release of thousands of pages of previously classified documents by Wikileaks was – probably like many people – outrage. But then we had some time to think about the matter. At the same time, we happened to be reading Jon Krakauer’s book on the life of the late Pat Tillman, Where Men Win Glory. Readers will remember Mr. Tillman as a star professional football player who took a leave of absence from his playing career to join the military after 9-11. He felt an obligation to serve his country after it was attacked on that tragic day a decade ago. The government used Mr. Tillman’s selfless act as both a recruiting tool and a patriotic rallying cry in the war against terrorism in Iraq and Afghanistan. Mr. Tillman entered military training and ultimately was sent to fight in Afghanistan. Ironically – and tragically – he saw very little actual combat action before being killed by other American soldiers in an incredibly stupid incident of “friendly fire “ that is detailed by Mr. Krakauer in excruciating and gory detail. Compounding both the tragedy and stupidity of Mr. Tillman’s death was what happened afterward.

Enormously embarrassed by the cause of Mr. Tillman’s death, and fearing a major propaganda defeat were the truth about his death to be disclosed, U.S. military and political leaders reaching as high as the White House engaged in an elaborate cover-up to conceal from the American public as well as from Mr. Tillman’s widow and family the true cause of his death. More than six years later, the loss of this idealistic and courageous young man seems even more tragic and pointless in view of the fact that it came in an Afghan military campaign that has been rife with strategic and logistical snafus and was likely unwinnable in the first place.

The Pat Tillman story is a painful reminder that that so-called liberal democracies routinely lies to their people on a daily basis. We expect non-democratic governments to conceal the truth – they do not view transparency and truth-telling as one of the duties of government. But democracy is supposed to be different. And yet in practice it isn’t even close. So-called liberal democracies lie about everything – domestic politics, foreign affairs, war, economics - everything. And the more significant the event and the higher the stakes, the bigger the lie.

John Farmer, counsel to the 9/11 Commission, wrote the following about what the U.S. government told the American people about the events of that tragic day: “In the course of our investigation into the national response to the attacks, the 9/11 Commission staff discovered that the official version of what had occurred that morning – that is, what government and military officials had told Congress, the Commission, the media, and the public about who knew what when – was almost entirely, and inexplicably, untrue.”5 Mr. Farmer’s book goes on to explain what he initially describes as “inexplicable” – the reason the American people were not told the truth about the events of 9/11 is that their government deliberately lied to them.

Now we have a self-appointed organization that operates in unregulated cyberspace that has taken upon itself to disclose the truths that governments do not want disclosed. Wikileaks is not expressing opinions; it is disclosing raw data in the form of original source documents from which readers can draw their own conclusions. While many of these documents are deemed to be “classified,” their disclosure has made a mockery of the entire concept of protecting documents from public disclosure. Other than those documents that disclose military secrets and/or place individuals’ lives in danger, which clearly should not be disclosed, many of the disclosed documents amount to little more than diplomatic or political gossip. Having reflected on what Wikileaks has done, I find it extremely disturbing that the media and public appear to be far more outraged by an individual or organization attempting to force governments to tell the truth than by the incessant efforts of governments to conceal the truth from the governed.

Before simply condemning what Wikileaks is doing, we should remind ourselves that Wikileaks is fulfilling the role that a free press in a truly free society should be fulfilling. The American media (and much of the Western media) has been completely co-opted by the financially-driven political power structure into repeating a narrative that is false and serves the interests of a small political-financial elite. Combating such a regime requires disrupting the status quo and upsetting established interests, which is precisely what Wikileaks is doing.

True liberal democracy is a messy and inefficient form of government, and Wikileaks is playing an essential role in the democratic process of shining a light on the actions of governments. It may be going too far in some instances (as noted above, disclosing military secrets or the identity of operatives whose lives could be put in danger is clearly inappropriate), but the lion’s share of the information being released deserves to see the light of day. Much of this information may be embarrassing, but it is not going to get anybody killed. Maybe its disclosure will raise the level of diplomatic discourse and hold governments to account, which can only be a good thing.

Some may say that Mr. Assange is taking it upon himself to second guess the government and those who know better than he what should be disclosed to the public. That may very well be true. But allowing governments to control the flow of information can only sow the seeds of tyranny. It is a profoundly sad commentary on the state of the world today that the public and media are far more eager to crucify Mr. Assange than to speak out against the bold-faced lies of their public servants and business leaders. Wikileaks may make us uncomfortable – in some cases excruciatingly uncomfortable - but that is exactly the point, isn’t it?

Michael E. Lewitt

[email protected]

January 5, 2011

5. John Farmer, The Ground Truth: The Untold Story of America Under Attack on 9/11 (New York: Penguin Group, 2009), p. 2.

Disclosure Appendix

This publication does not provide individually tailored investment advice. It has been prepared without regard to the circumstances and objectives of those who receive it. This report contains general information only, does not take account of the specific circumstances of any recipient and should not be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. Each recipient should consider the appropriateness of any investment decision having regard to his or her own circumstances, the full range of information available and appropriate professional advice. Harch Capital Management, LLC recommends that recipients independently evaluate particular investments and strategies, and encourage them to seek a financial adviser’s advice. Under no circumstances should this publication be construed as a solicitation to buy or sell any security or to participate in any trading or investment strategy, nor should this publication or any part of it form the basis of, or be relied on in connection with, any contract or commitment whatsoever. The value of and income from investments may vary because of changes in interest rates or foreign exchange rates, securities prices or market indexes, operational or financial conditions of companies, geopolitical or other factors. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. The information and opinions in this report constitute judgment as of the date of this report, have been compiled and arrived at from sources believed to be reliable and in good faith (but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness) and are subject to change without notice. Harch Capital Management, LLC and/or its employees, including the author, may have an interest in the companies or securities mentioned herein. Neither Harch Capital Management, LLC nor its employees, including the author, accepts any liability whatsoever for any loss or damage arising from any use of this report or its contents. All data and information and opinions expressed herein are subject to change without notice.

The HCM Market Letter

Michael E. Lewitt, Editor

The HCM Market Letter is published on a monthly basis by The HCM Market

Letter, LLC. Offices at 751 Park of Commerce Drive, Suite 118, Boca Raton, FL, 33487. Telephone (561) 226-6199; Fax (561) 995-4946. Delivery is by electronic mail. Annual subscription rate is $395 for individuals and $995 for institutions. Visit our web site at www.hcmmarketletter.com. Copyright warning and notice: It is a violation of federal copyright law to reproduce or distribute all or part of this publication to anyone (with the exception of individuals within the same institution pursuant to the subscription agreement) by any means, including but not limited to photocopying, printing, faxing, scanning, e-mailing, and Web site posting without first seeking the permission of the publisher. The Copyright Act imposes liability of up to $150,000 per issue for infringement. Information concerning possible copyright infringement will be gratefully received.

Read more articles by Michael Lewitt