Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

When you’re ready for a meal of assorted chopped up pieces of meat, blended into a tightly wrapped package, you’ll often choose sausages. Just as shoppers will look for their favorite brand of sausage, investors select their benchmarks based on brand name, with Russell and S&P in the lead.

Only a few style-conscious consumers read the label, and that’s true in the grocery market and in the world of portfolio management.

But would we make the same choices if we knew which factors are combined to make these investment-world sausages? After all, the indexes we use affect our decisions every day. First and foremost, asset allocations are based on the style make-up of the market. For example, we might misallocate if some stocks are being called growth that could be better viewed as value. Moreover, performance evaluation relies heavily on comparisons to style indexes.

In the current financial crisis, the choice of factor largely dictates whether financial stocks are classified as value or growth. A Price/Book (P/B) factor assigns most financials to value, whereas the alternative three-factor model assigns financials to growth. Because financials are 16% of the market, this style assignment disagreement causes significant differences in performance between indexes that employ these disparate factors. Prior to the current crisis, both classification approaches agreed that most financials were value stocks.

Dissecting the popular index sausages

Russell and S&P use P/B to divide the universe of stocks into value and growth. High P/B is growth and low P/B is value. The idea is that a stock priced near its cost basis is inexpensive - a good value. But as Laurence Siegel states in a CFA Research Foundation monograph, “Book value is mostly a historical accident. It is the accounting profession’s estimate of the company’s value; it reflects what the company paid for assets…includes the goodwill of companies acquired.” Not all indexes, however, are constructed using P/B. Some use price/earnings ratios (P/E) combined with other factors like dividend yield.

P/E is a growth measure. Investors will pay more for current earnings if they expect those earnings to grow. Dividend yield is a value measure, since dividends are generally paid by companies with established product lines who would rather pay out earnings to shareholders than invest in new projects. The idea of using both a value and a growth measure is that one confirms the other. A high P/E and a low yield signify growth, just as a low P/E and high yield indicate value. Stocks with offsetting value-growth characteristics generally fall in a middle section we call “Core.”

Some researchers use P/E, yield and forecast earnings growth to predict the equity risk premium. Stock prices are forecast to grow according to the following formula:

Growth = Dividend yield + earnings growth + Price/Earnings expansion or contraction

Price/Book does not enter into this forecast. The three-factor model incorporates two of the three factors that affect future stock prices, which should be a consideration in asset allocations.

Some say that it doesn’t matter much which factor is used because all style indexes behave alike: “When growth is in favor all of the growth indexes are in favor, and the same for value.” This is simply not true. Style indexes behave differently primarily because of the factors used to classify stocks, as is evident by comparing the Russell and Surz index families.

The Russell indexes use P/B to create six style indexes: large, middle and small indexes for value and growth. The Surz Style Pure® (SSP) Indexes use three factors – P/E, dividend yield and normalized (by sector) P/B – to create nine indexes: large, middle, small indexes for value, growth and core, where “core” is defined as the stocks in between value and growth. Russell deals with “core” by assigning these stocks in the middle to both value and growth.

These differing constructs cause Russell and SSP to differ along many dimensions, including performance, characteristics (such as capitalization, P/E, yield, etc.), and stock composition. We’ll start with stock composition. My firm, Insider Analytics has announced the release of Style Scan (see here), a tool to visualize the stock make-up of individual portfolios. Every stock in the portfolio is plotted in two dimensions, where the x-axis represents value (left)-growth (right) and the y-axis represents company size (capitalization). In this way, every portfolio has a unique “style signature” – the graphic display of each constituent based on these two dimensions.

Visualizing indexes using Style Scan

Style Scan shows that the style definitions that are used to scale the X-axis dramatically affect this signature. Specifically, many stocks have a significantly different X (value-growth) coordinate when using P/B versus three-factor models.

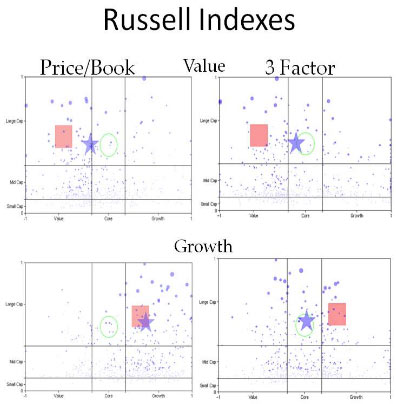

The single-factor P/B-based framework renders a completely different signature than the three-factor model used by SSP. This is shown graphically in the next two exhibits. Let’s start with the signatures of the Russell 1000 (large cap) Value and Growth indexes.

The graph in the upper left shows that, using the single-factor P/B framework the constituents of the Russell 1000 Value index cluster in the upper left of the graph, which is the large value sector. The centroid of the constituents, indicated by the star, also plots toward the upper left. The square in the exhibit indicates where we expect the star to plot; it is in the center of the upper left quadrant. The green circle is the centroid for the entire market. The same clustering is more evident with the Russell 1000 Growth index, with a purer position in the upper right quadrant of the graph on the lower left.

But if we analyze the stocks in the Russell indexes using a three-factor model, the message is totally different; the constituent stocks are broadly dispersed over the style space, and the index centroid in the middle of the graph. Using the P/B factor model, the points cluster exactly where they should along the X (value-growth) axis, but these same stocks are scattered all over style space when that space is defined by the three-factor model. The single- and three-factor models tell radically different stories.

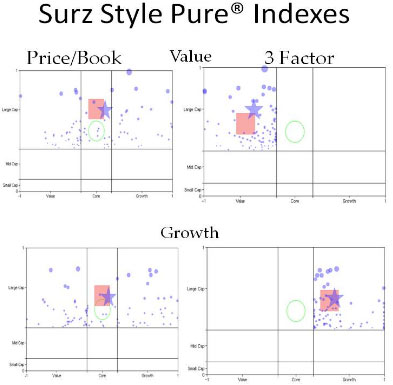

A similar result occurs if we look at the SSP indexes. Using the three-factor model, its constituents cluster as expected, but fall all over the map when P/B is used as the classification variable. This is true for both the SSP large value and large growth indexes, as shown in the graphs on the right.

The construction of the grids in Style Scan is described here. For the U.S. analyses we start with the entire Compustat database of approximately 5,000 stocks. These are divided into three size groupings based on capitalization. Large is the top 65% of the universe, mid is the next 25% and small is the bottom 10%. Then we sort within each size group by the classification factor, either P/B or three-factor. The top 40% by count are assigned to value, the bottom 40% to growth, and the 20% in the middle to core.

Style Scan lets you choose your classification factors: P/B or three-factor. But before you choose, you’ll want to know a little more about the implications for portfolio characteristics and performance.

The value of Style Scan is in controlling portfolio compositions, by seeing concentrations and voids, and in comparing portfolios of managers that you may want to employ. These inferences are dramatically affected by your choice of classification variable, so it’s helpful to understand the “lens” you’re using to view the world. The characteristics of stocks in each style sector calibrate this view.

Lessons from Q3 of 2008

The characteristics of the large value and large growth sectors in the third quarter of 2008 illustrated the key differences between the P/B and three-factor models:

Company size: P/B “sees” growth companies being larger than value. Three-factor sees the opposite.

P/E ratio: P/B “sees” growth companies as having lower P/Es than value. Three-factor sees very much the opposite because P/E is one of the classification factors.

Yield: Both “see” value as higher yield.

P/B ratio: Of course, the P/B-based classification renders growth with higher P/B than value. Although the three-factor model includes P/B, the other factors dominate, and value has higher P/B.

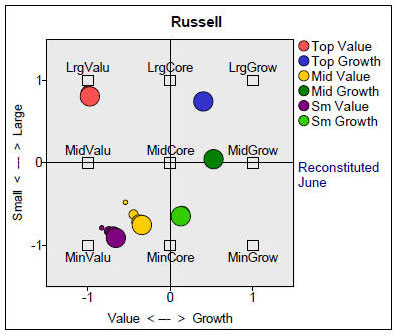

Finance allocation: The large company finance sector of the U.S. stock market is currently $1.3 Trillion. More than $1 Trillion, or about 90% of the dollars in Finance are classified as value using the P/B definition, versus 20% with the three-factor model, which places most of Finance in growth. This substantial difference reflects the current economic crisis, and in particular the view of the three-factor model regarding negative P/Es.

The three-factor model views stocks with negative P/Es as growth stocks. One way to visualize this rationale is to consider the reciprocal of P/E, which is the earnings yield. As shown in the exhibit, there is a continuum in the earnings yield, along the definition of growth stocks, as earnings become negative. By contrast if you are using P/E ratios, there is a discontinuity when you try to classify stocks with negative earnings.

Now let’s look at the return behavior of the two different classification schemes. The next exhibit, courtesy of Wianno Associates, plots the Russell indexes against the SSP indexes using returns-based style analysis. There are some performance similarities, particularly in large and small value styles, but for the most part the two definitions behave differently.

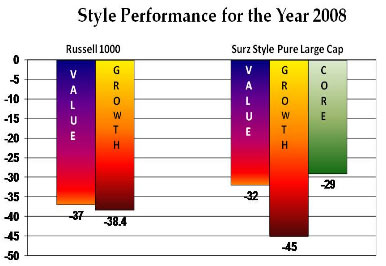

Another example is provided by last year’s decline, as shown in the next exhibit. The Russell large value and large growth indexes both lost about the same in 2008, whereas the SSP growth underperformed both value and core. Importantly, core defended best, a fact that has gone virtually unrecognized.

Core is important for portfolio construction and performance evaluation. As you can see in the exhibit, three-factor-type growth managers were penalized if compared to the Russell growth index, whereas value managers were rewarded. As the active-passive debate continues, we need to fine tune our benchmarks because we need a better handle on who is winning and who is losing.

Conclusion

It matters a lot which factors are used to define stock style classifications. Different approaches not only assign stocks to different styles, but they result in financial characteristics and performance behaviors that are materially different. It’s important to know the ingredients of your style sausages, and not just select them based on brand name.

Read more articles by Ron Surz