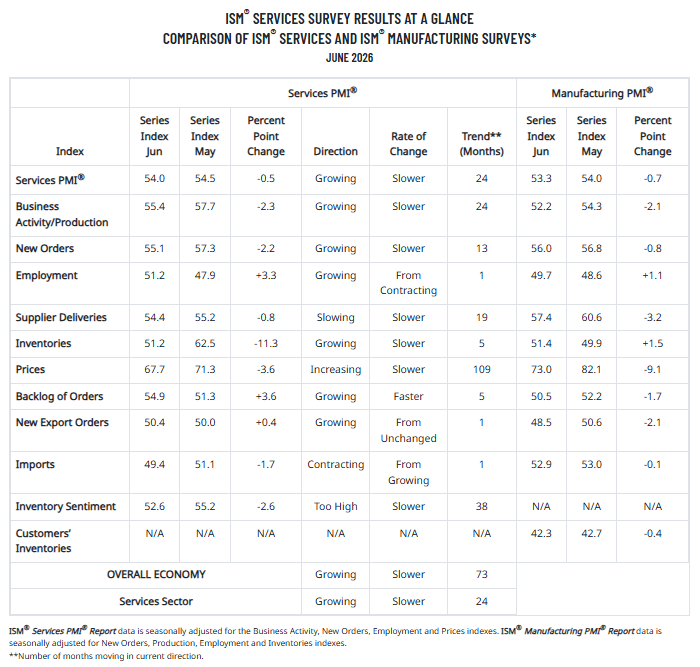

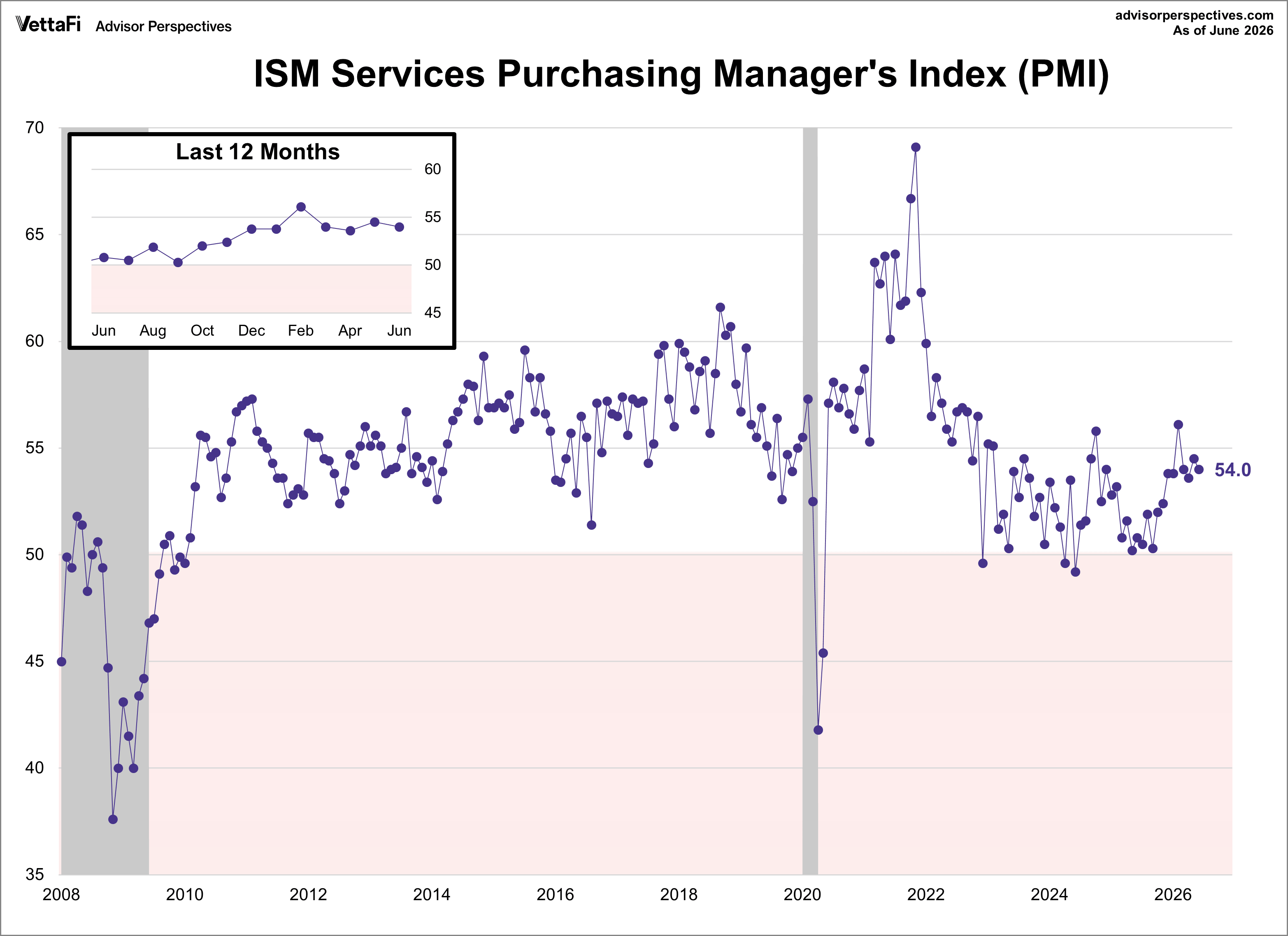

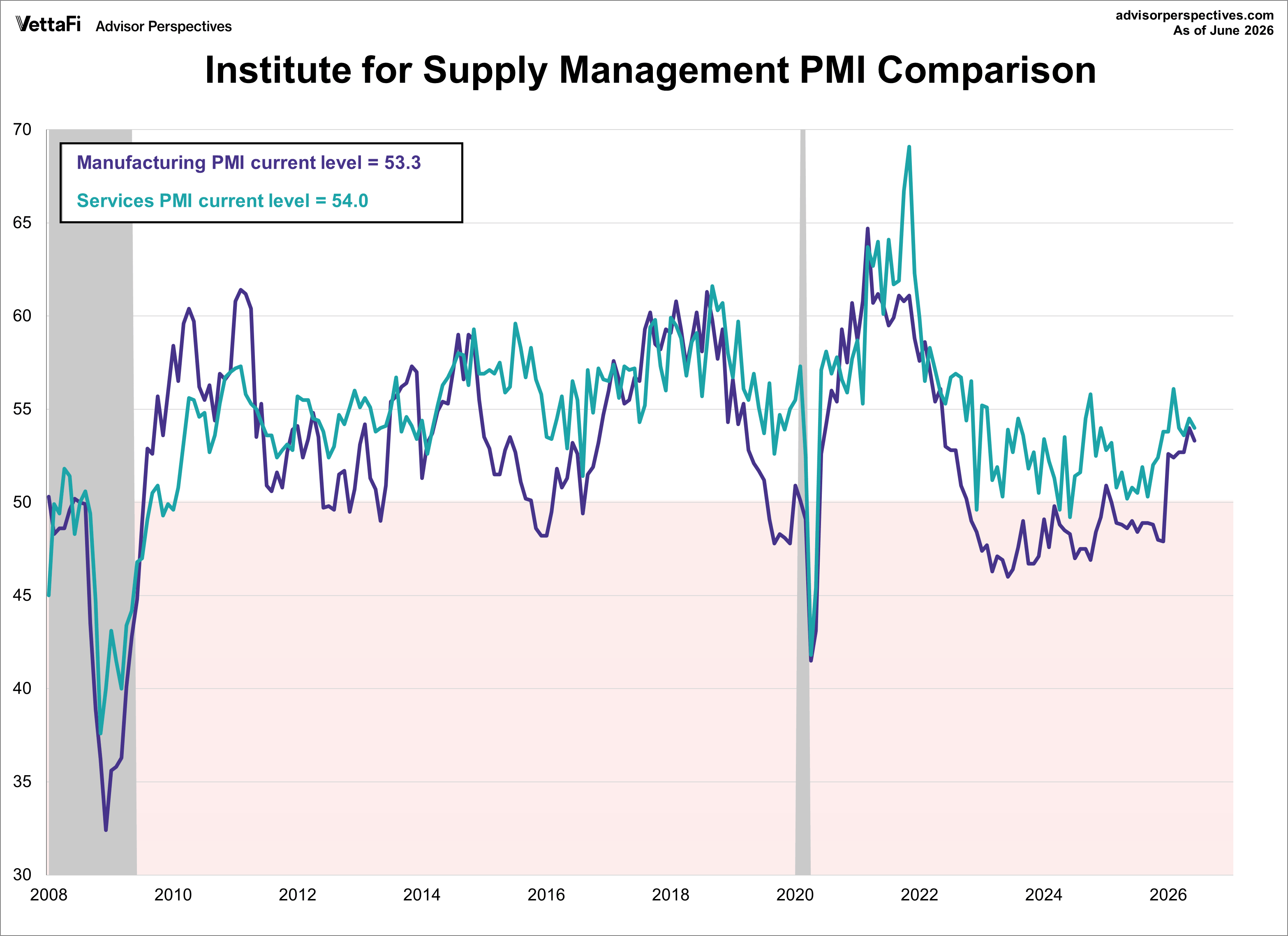

The Institute for Supply Management (ISM) released its June Services Purchasing Managers' Index (PMI), with the headline composite index at 54.0. This was slightly lower than the forecast of 54.2 but keeps the index in expansion territory for a 24th consecutive month.

Here is an excerpt from the report summary:

Miller continues, “The Prices Index decreased to 67.7 percent, its lowest reading since February 2026 (63 percent). In this month’s report, some respondents reported reduced prices paid for gasoline and diesel, but this was not seen across the board. Petroleum-related products were mentioned again as a commodity up in price, something that we expect to see for several months as higher oil prices work their way through the supply chain, but they should ease off in the fall assuming recent progress in moving oil through the Strait of Hormuz continues. As of late June, West Texas Intermediate crude oil dropped below US$70 per barrel for the first time since February, a more than 30 percent drop from its high in recent months. The Supplier Deliveries Index continued to indicate slower performance; while easing for its second month in a row, it is still above its 12-month average.

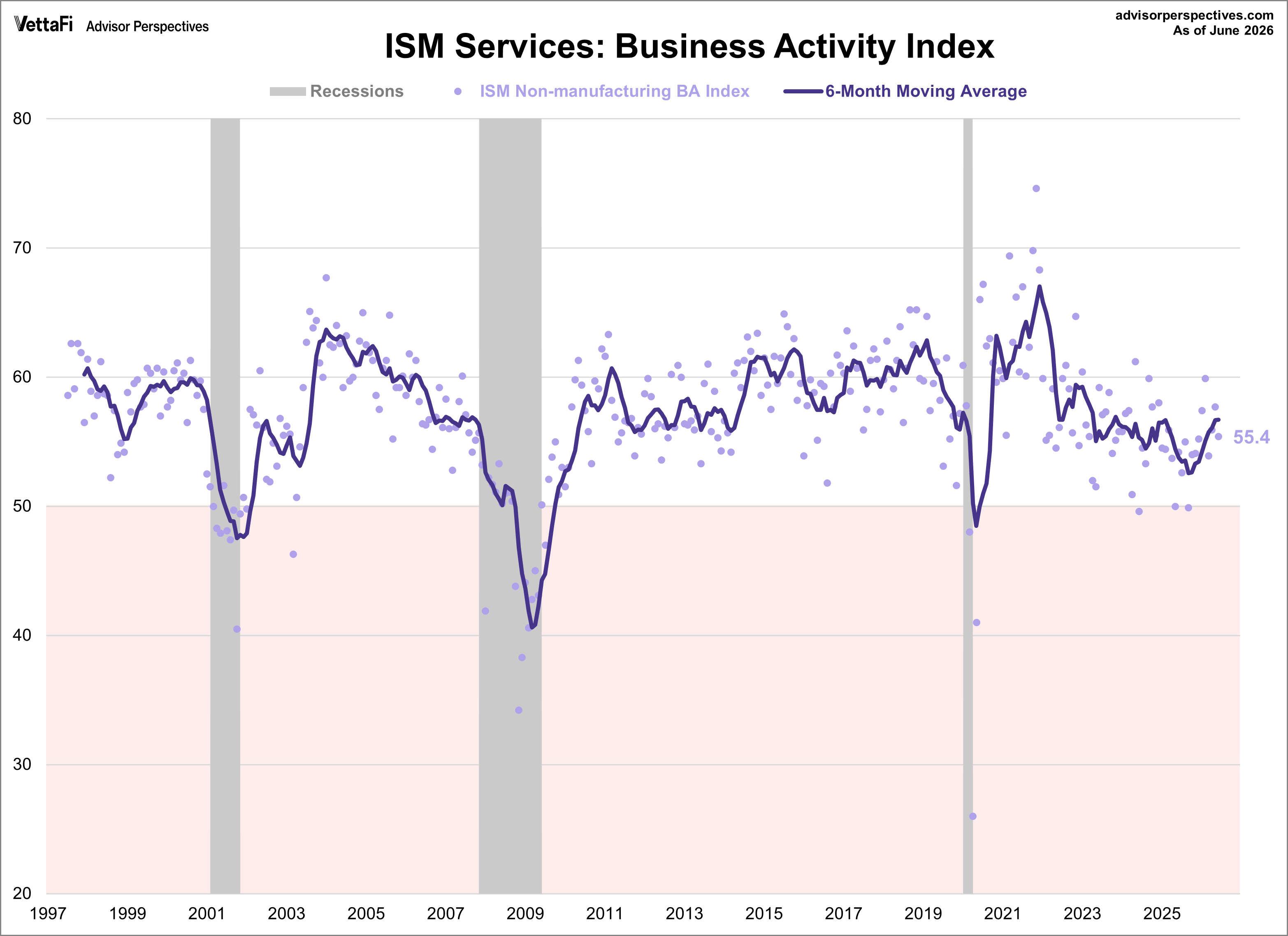

“The more than 2-percentage point drops in both the Business Activity and New Orders indexes were partially offset by the 3.3 percentage point increase in the Employment Index. All four subindexes of the Services PMI® are once again in expansion territory and above their 12-month averages. In a welcome sign of reduced growth rate of prices paid, June’s Prices Index reading of 67.7 percent is its lowest in four months and below its 12-month average. There were fewer commodities reported as up in price compared to previous months.

“Despite easing of the Supplier Deliveries Index, there was an increase in commodities listed as ‘in Short Supply,’ increasing from five in May to nine in June. All commodities in short supply in June are commodities necessary for data center construction, while the Utilities and Information industries all continued their more than six-month runs in expansion territory. Memory components, copper, aluminum, and heating, ventilation and air conditioning (HVAC) equipment continued multimonth runs of being listed as up in price.

“Respondents in June commented less frequently about pricing impacts on petroleum products, while tariff impacts continued to be a theme for increased pricing pressure. The Inventories Index dropped to its second-lowest level since October 2025, indicating that the buy-ahead phenomenon from earlier in the year may be over. The Imports Index dropped into contraction territory for the first time in five months, down from a spike to 55.2 percent in March, its highest level in over two years. The Backlog of Orders Index reached its second-highest level in almost four years. These readings, taken with respondent commentary, seem to indicate that supply chains are stabilizing amid sustained business activity, giving confidence to businesses that selective, yet modest, increased employment is warranted. World Cup-related hiring in the U.S. likely contributed to the increase to the Employment Index. Of the 18 services industries, nine of them — representing over 58 percent of U.S. gross domestic product (GDP) — reported higher employment levels in June. This represents widespread confidence that hiring is again warranted to support activity levels.”

Here is a table showing the PMI's components.