The Buffett Indicator, also known as Market Capitalization to GDP Ratio, is a long-term valuation indicator for stocks that has become popular in recent years, thanks to Warren Buffett. Back in 2001, he remarked in a Fortune Magazine interview that "it is probably the best single measure of where valuations stand at any given moment." It is a measure of the total market value of all publicly-traded stocks in a country divided by the country's GDP and can be used as a way to assess whether the country's stock market is undervalued, fair valued, or overvalued.

Key Takeaways

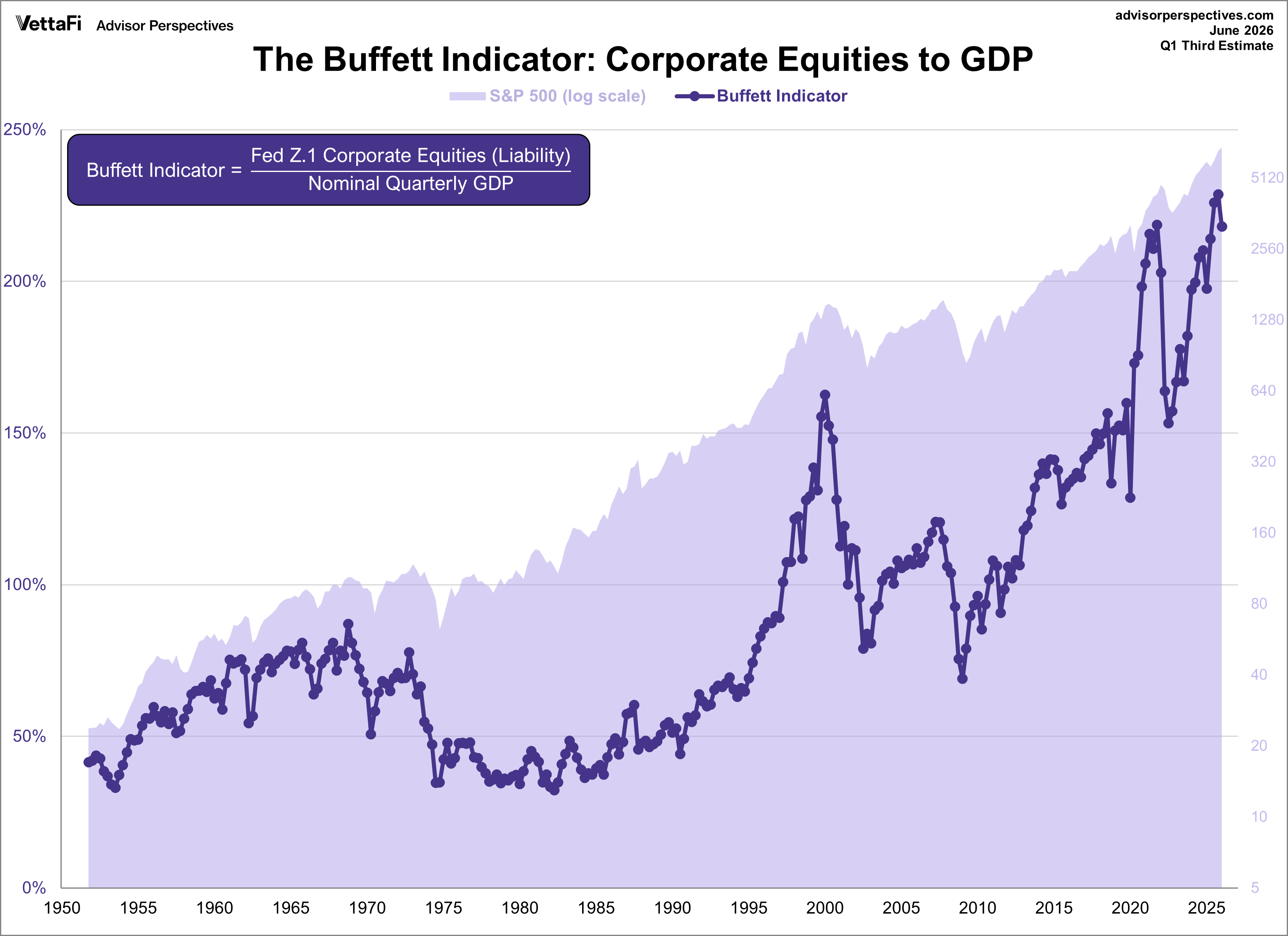

- The Buffett Indicator reached 218.1% in Q1, standing 56.6% above its trendline and signaling an overvalued stock market.

- The FT Wilshire 5000 to GDP variant recorded a 214.1% valuation, using concurrent data to eliminate lagging distortions.

- The Buffett Indicators tracks long-term stock valuations but remains ineffective for short-term market timing against the S&P 500.

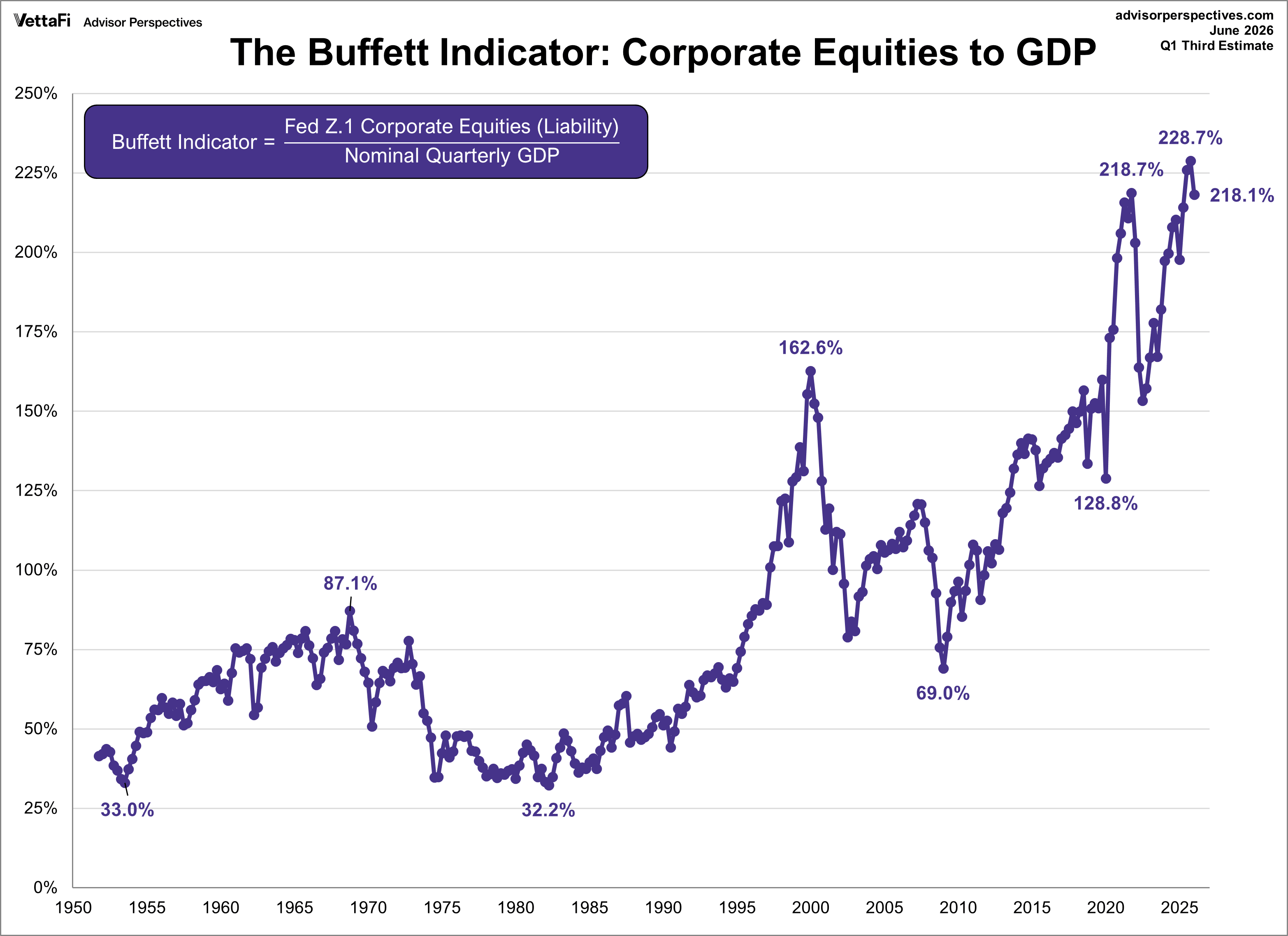

The four valuation indicators we track in our monthly valuation overview offer a long-term perspective of well over a century. The raw data for the "Buffett Indicator" only goes back as far as the middle of the 20th century. Quarterly GDP dates from 1947, and the Fed's balance sheet has quarterly updates beginning in Q4 1951. With an acknowledgment of this abbreviated timeframe, let's take a look at the plain vanilla quarterly ratio with no effort to interpolate monthly data.

Buffett Indicator: The Latest Data

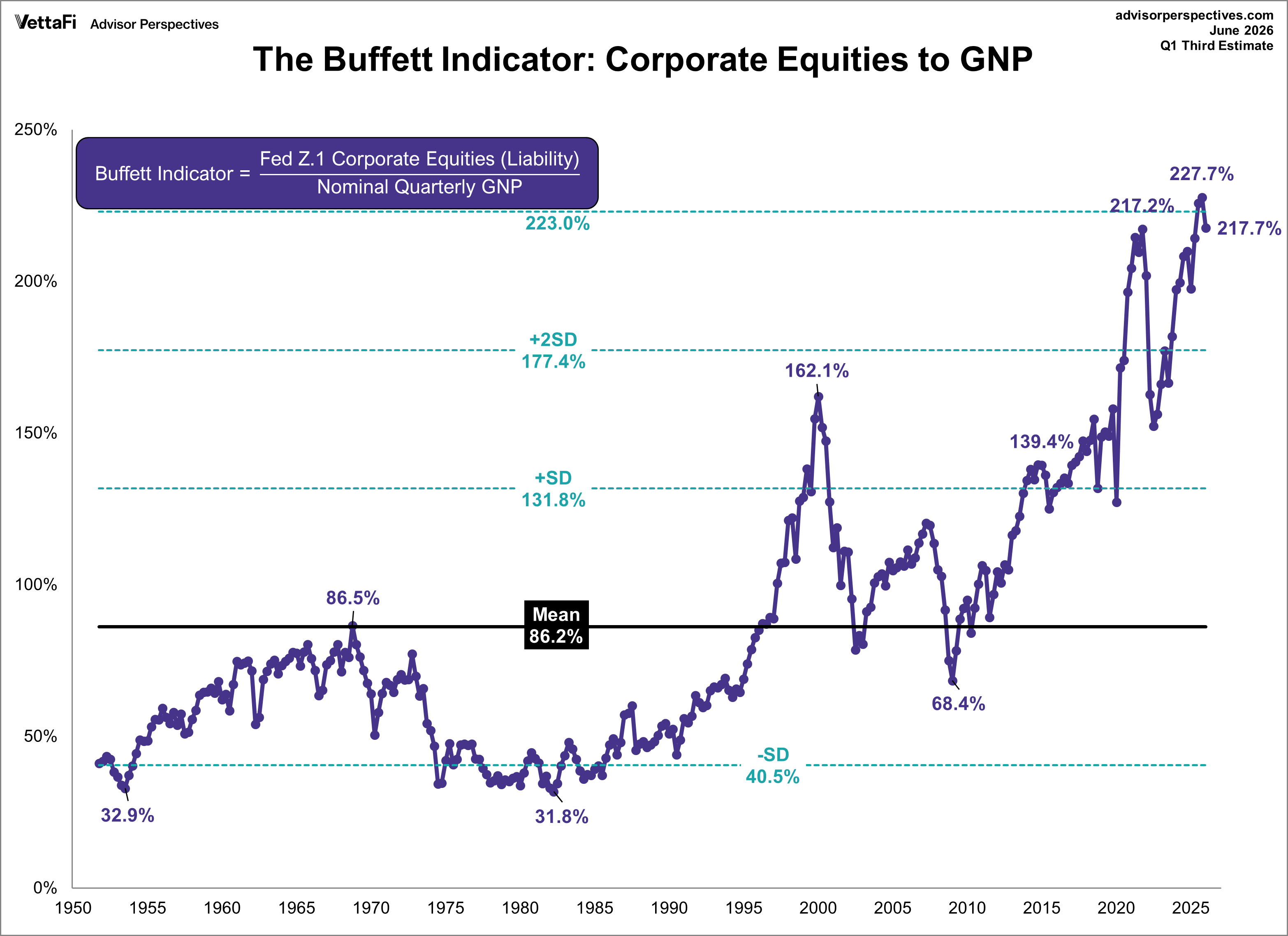

Following the Q1 GDP third estimate, the 'Buffett Indicator'—the ratio of corporate equities to GDP—now stands at 218.1%. This marks the fourth-highest reading in history. Thus, the indicator is signaling an OVERVALUED market. Please note that this update follows GDP releases, which always lag.

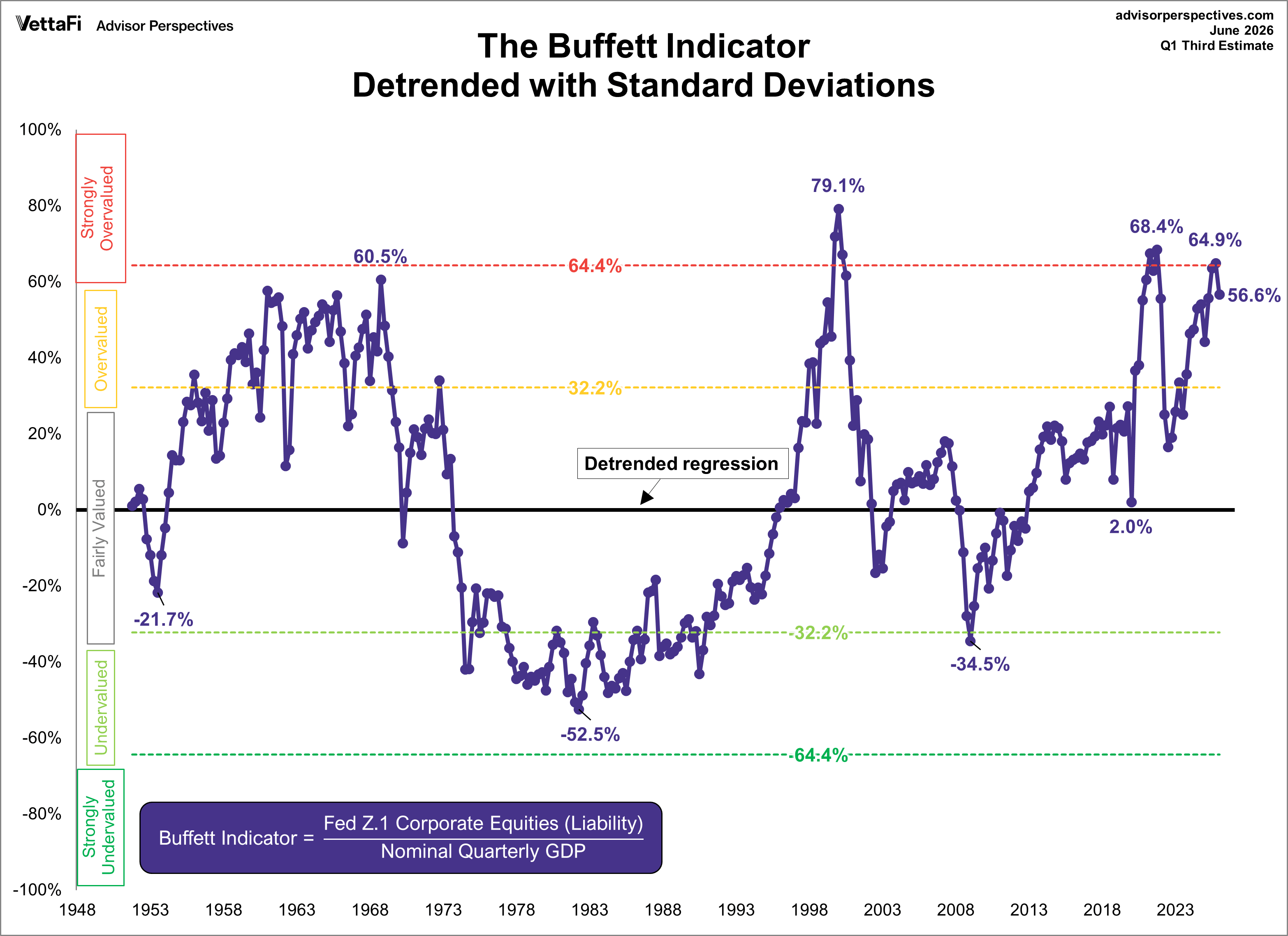

Buffett Indicator: De-trending the Data

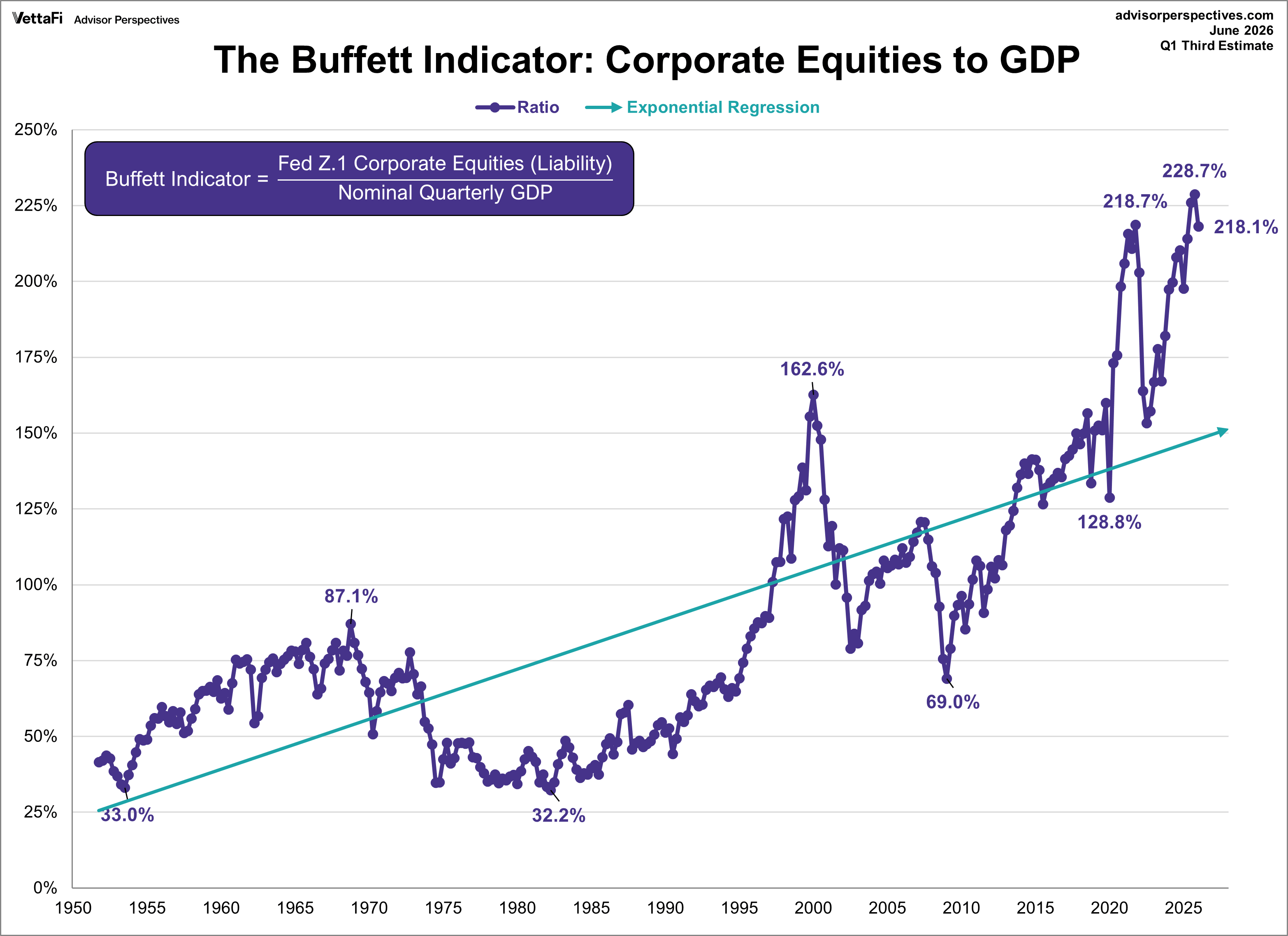

A conspicuous feature of the Buffett indicator is the upward trend over the decades since the start of the data series. For a better sense of valuation over time, let's de-trend the data by letting Excel draw a regression through the series and eliminating the upward trend. First, let's draw the regression through the series.

Now let's de-trend and add standard deviations.

The current Buffett Indicator value of 218.1% is 56.6% above its trendline (1.8 standard deviations), indicating the market is OVERVALUED.

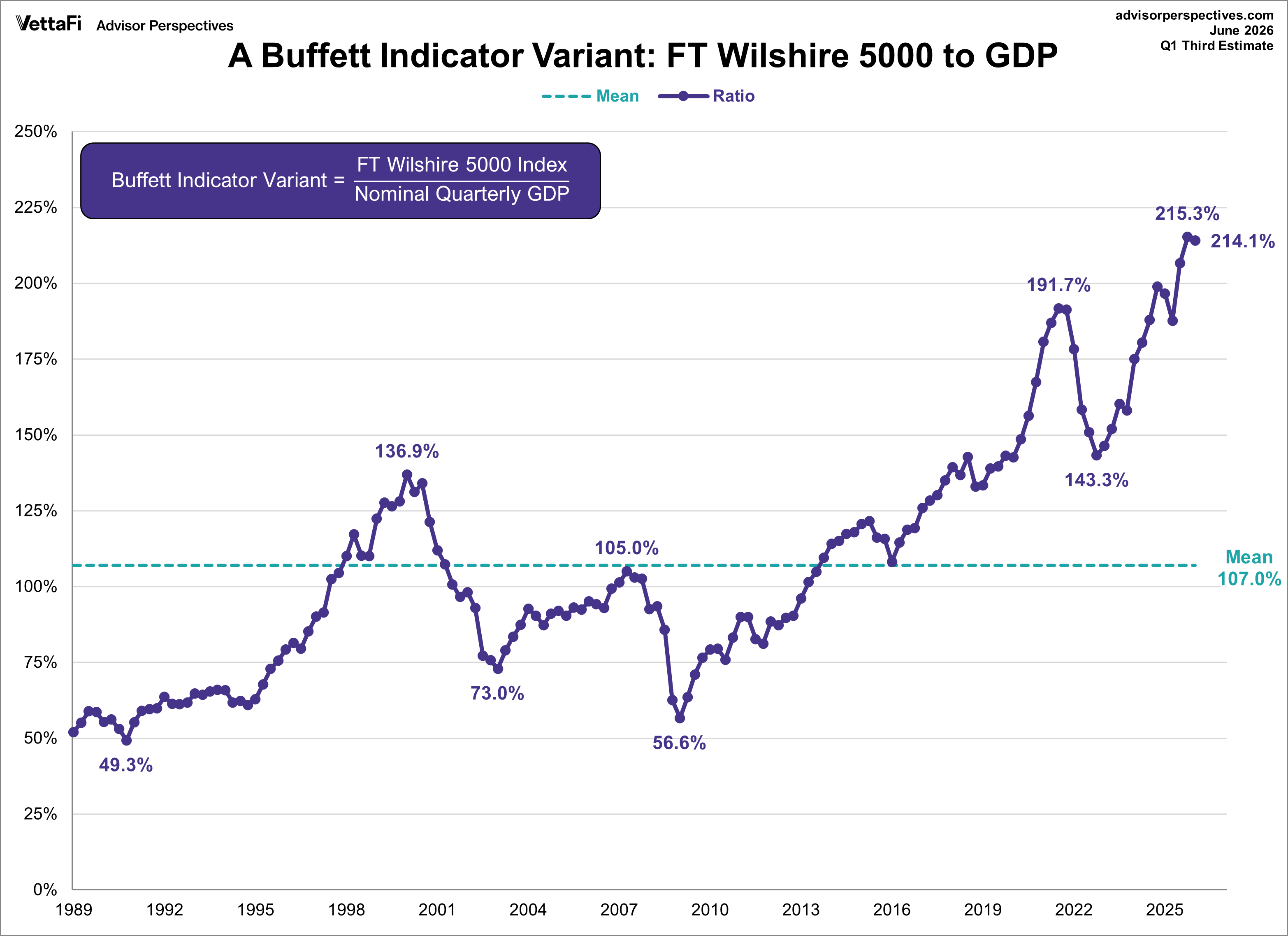

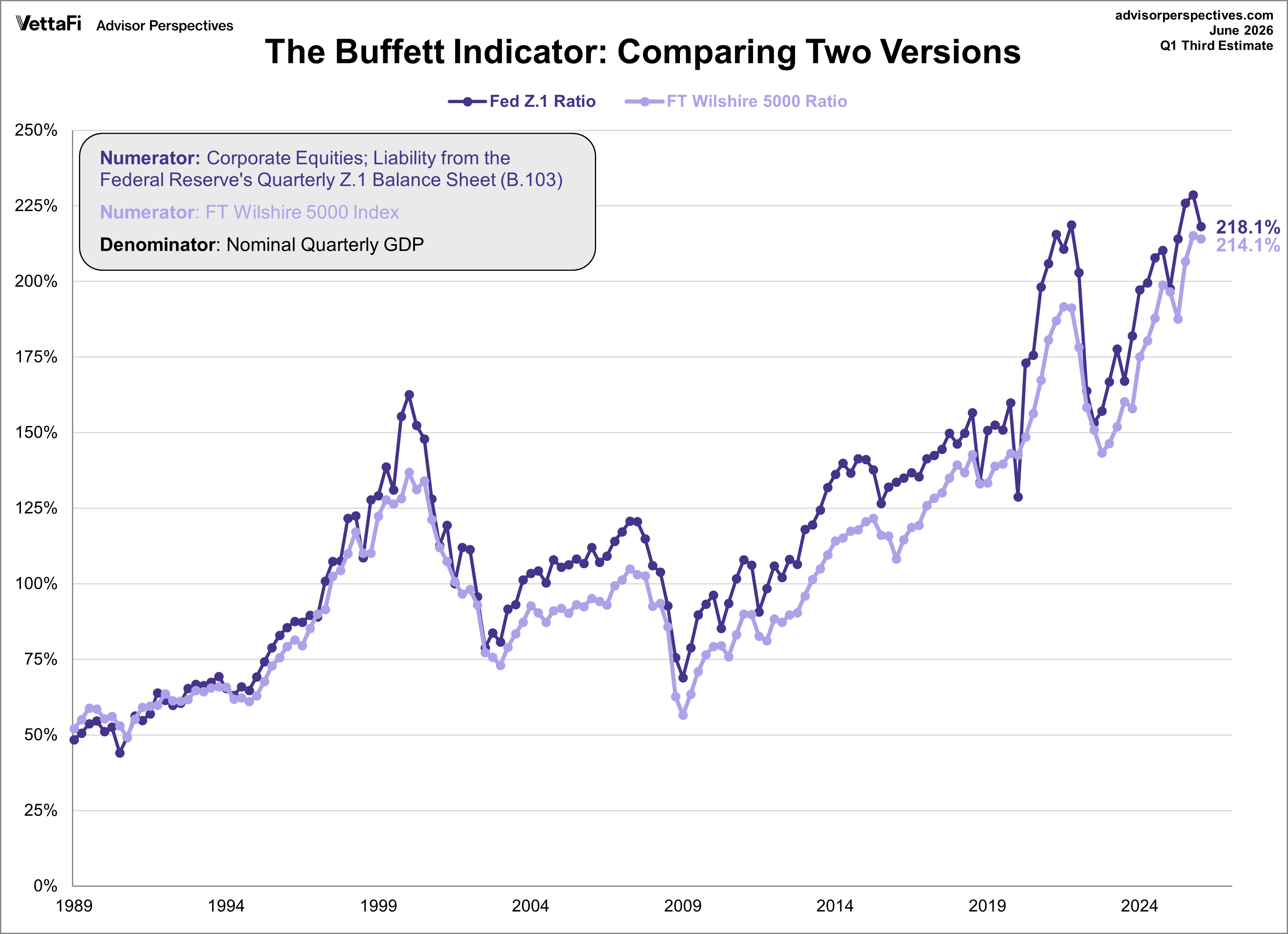

Buffett Indicator Variant: FT Wilshire 5000 to GDP

Here is a more transparent alternate snapshot over a shorter timeframe using the FT Wilshire 5000 Price Index divided by GDP. The Wilshire index is a more intuitive broad metric of the market than the Fed's rather esoteric "nonfinancial corporate business; corporate equities; liability, level". I've noticed some folks use lagging GDP figures to estimate the current Buffett indicator figures - in other words, people have used the current numerator and the lagging GDP figure in the calculation, which is not accurate. I have chosen to use data from the concurrent time period for all series.

Using the FT Wilshire 5000 as the numerator, the current Buffett Valuation Indicator is 214.1%, the second highest level in the series' history behind only the previous quarter.

A quick technical note: To match the quarterly intervals of GDP, for the Wilshire data I've used the quarterly average of daily closes rather than quarterly closes, slightly smoothing the volatility.

Buffett Indicator and FT Wilshire 5000: How well do the two views match?

The first chart above uses Fed data back to the middle of the last century for the numerator, the second uses the FT Wilshire 5000, the data for which only goes back to 1989. The Wilshire is the more familiar numerator, but the Fed data gives us a longer timeframe. And those early decades, when the ratio was substantially lower, have definitely impacted the trend.

To illustrate the point, here is an overlay of the two versions over the same timeframe. The one with the Fed numerator has a tad more upside volatility, but they're singing pretty much in harmony.

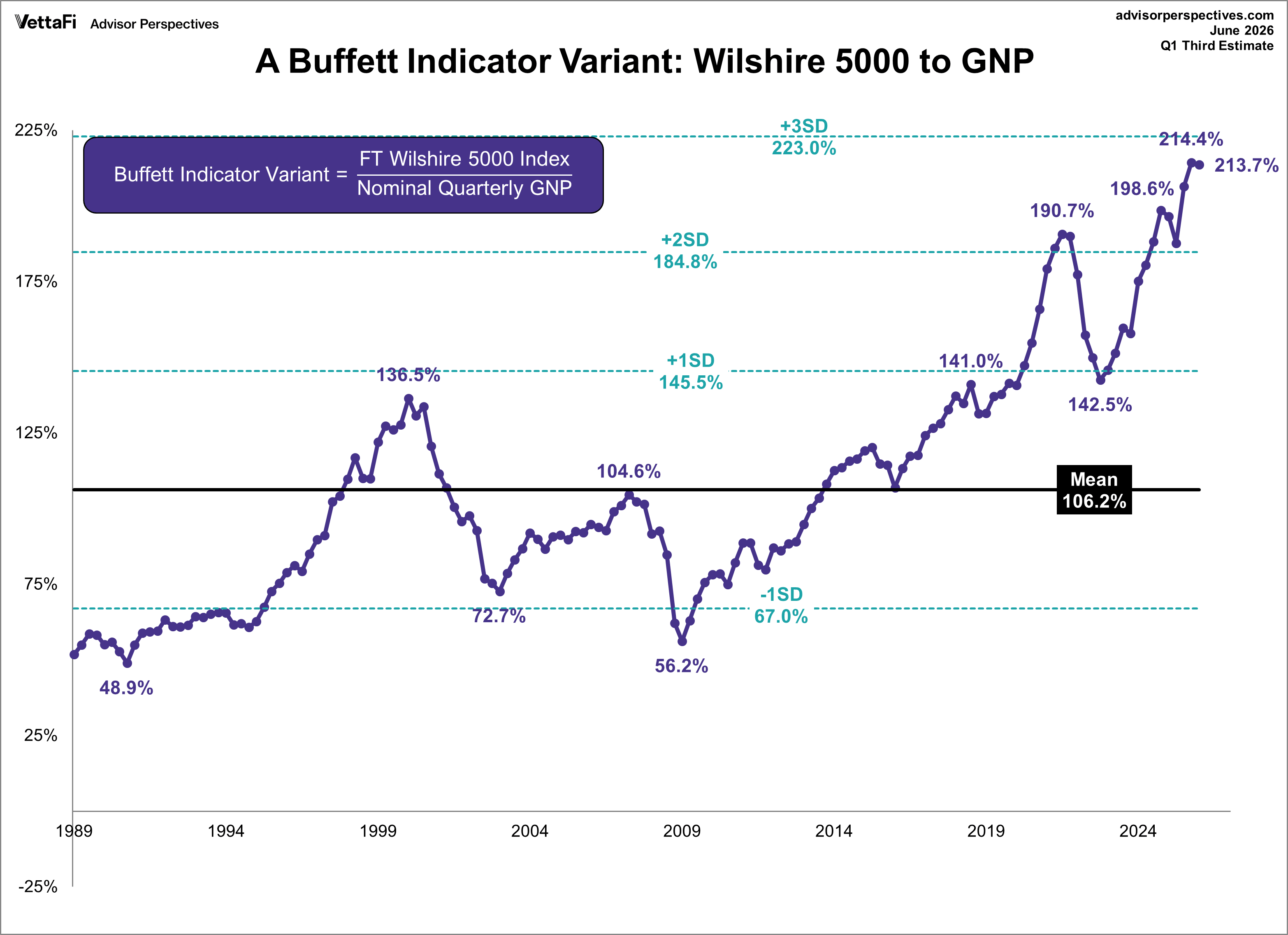

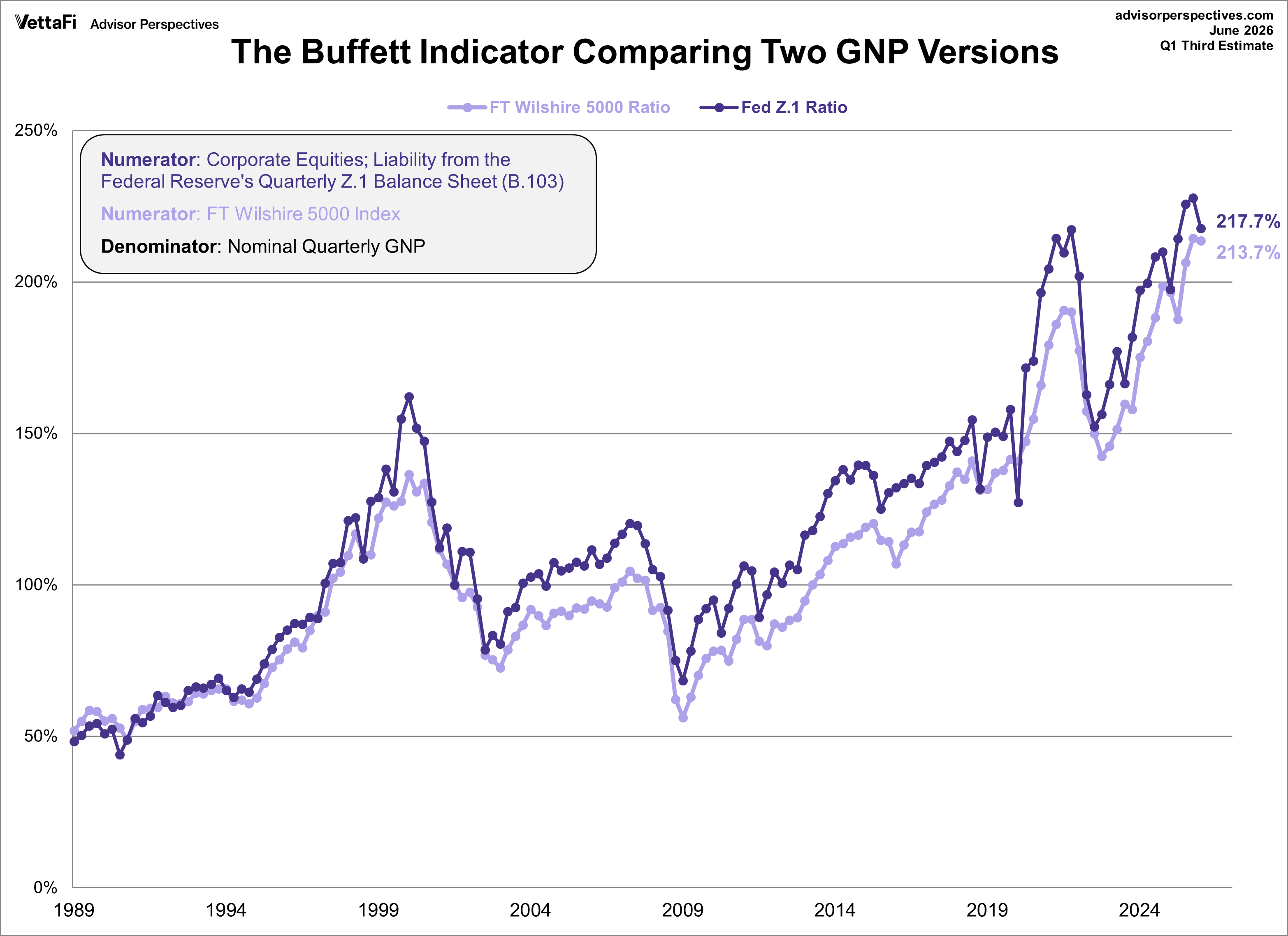

Buffett Indicator: Wouldn't GNP give a more accurate picture?

That is another question we've been asked many times. Here is the same calculation with gross national product (GNP) as the denominator; the two versions differ very little from their GDP counterparts.

Here is an overlay of the two GNP versions -- again, very similar.

Buffett Indicator: What do these charts tell us?

A question we're repeatedly asked is why we don't include the "Buffett Indicator" in the overlay of the four valuation indicators updated monthly. We've not included it for various reasons: The timeframe is so much shorter, the overlapping timeframe tells the same story, and the four-version overlay is about as visually "busy" as we're comfortable graphing.

One final comment: While this indicator is a general gauge of market valuation, it's not useful for short-term market timing, as this overlay with the S&P 500 makes clear.

Read more updates by Jen Nash