Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which it bases its decisions. This committee statement is about as close as it gets to identifying its method.

There is, however, a general belief that there are four big recession indicators that the committee weighs heavily in their cycle identification process. They are:

The Latest Indicator Data: Industrial Production

Industrial production rose less than expected in June, increasing 0.1% after May's 0.1% growth. This was lower than the expected 0.2% growth and marks a 1.1% increase compared to one year ago.

Here is a breakdown of the three major industry groups:

-

Manufacturing output was flat in June and up 1.1% year-over-year.

- The index for mining was up 0.4% in June and up 2.4% year-over-year.

- The index for utilities was up 0.4% in June and up 0.3% year-over-year.

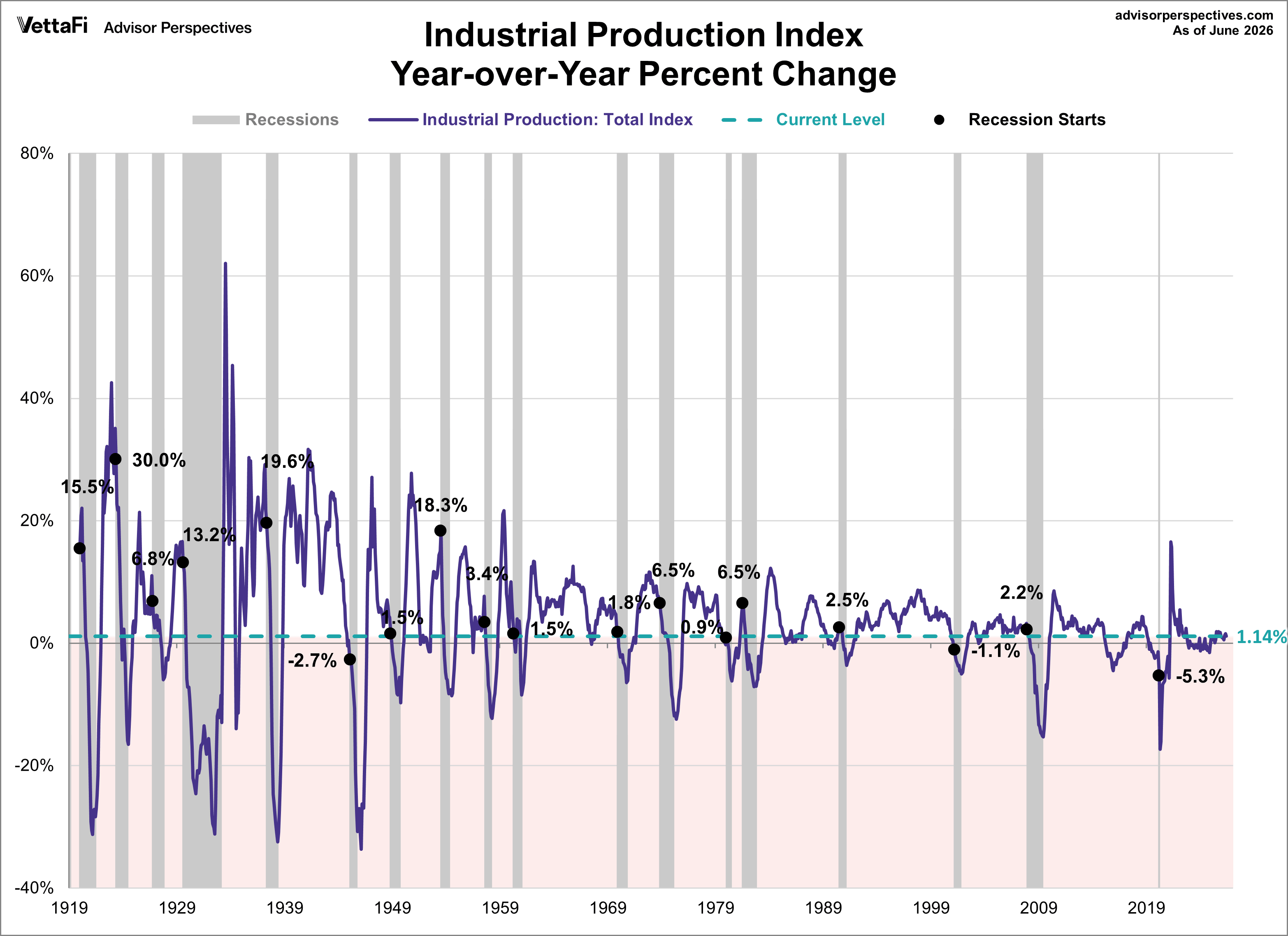

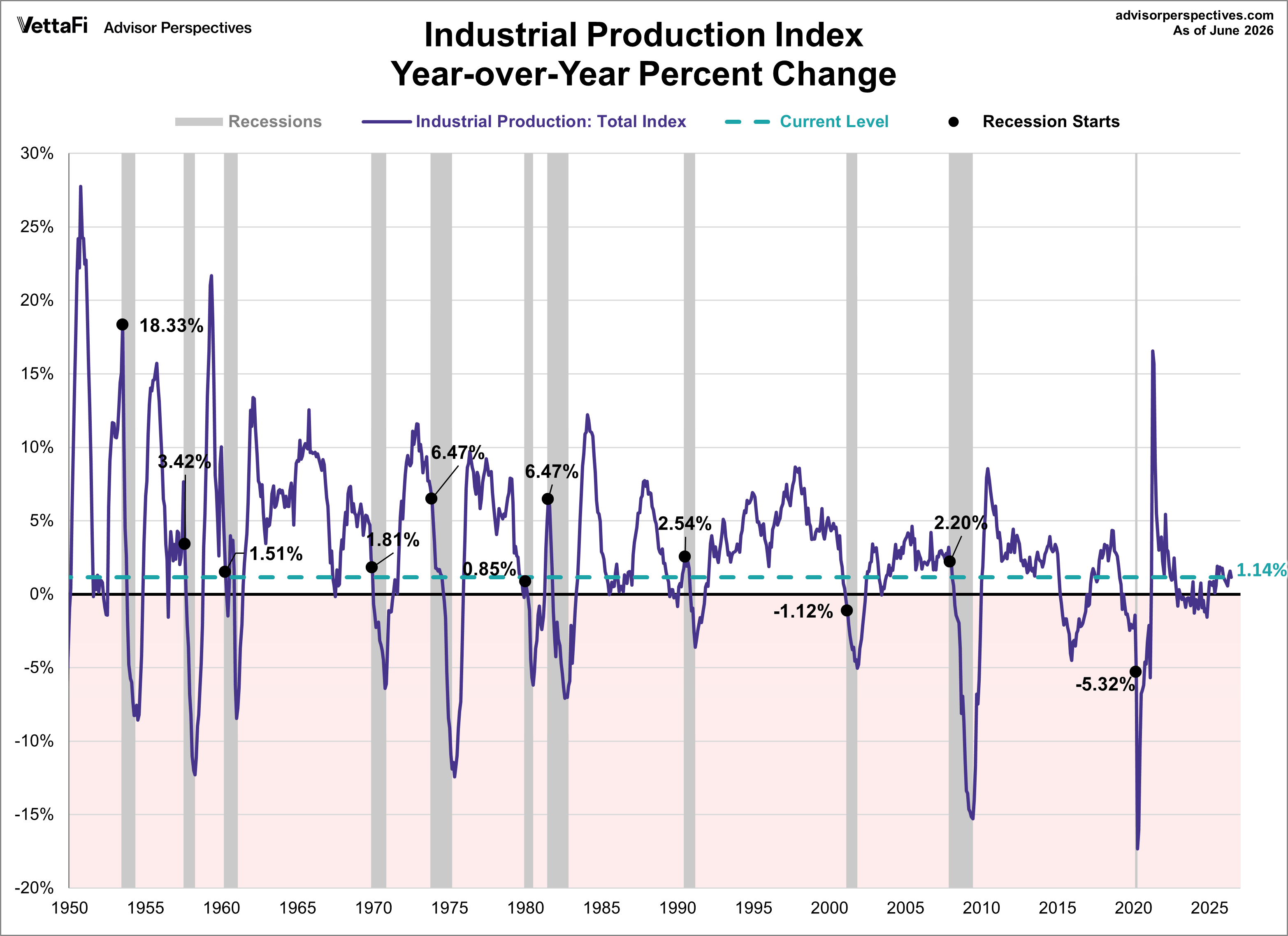

The chart below shows the year-over-year percentage change in industrial production since the series inception in 1919. The current level is at or lower than at the onset of 14 of 18 recessions over this time frame of nearly a century.

Industrial Production: Visualizing the Data

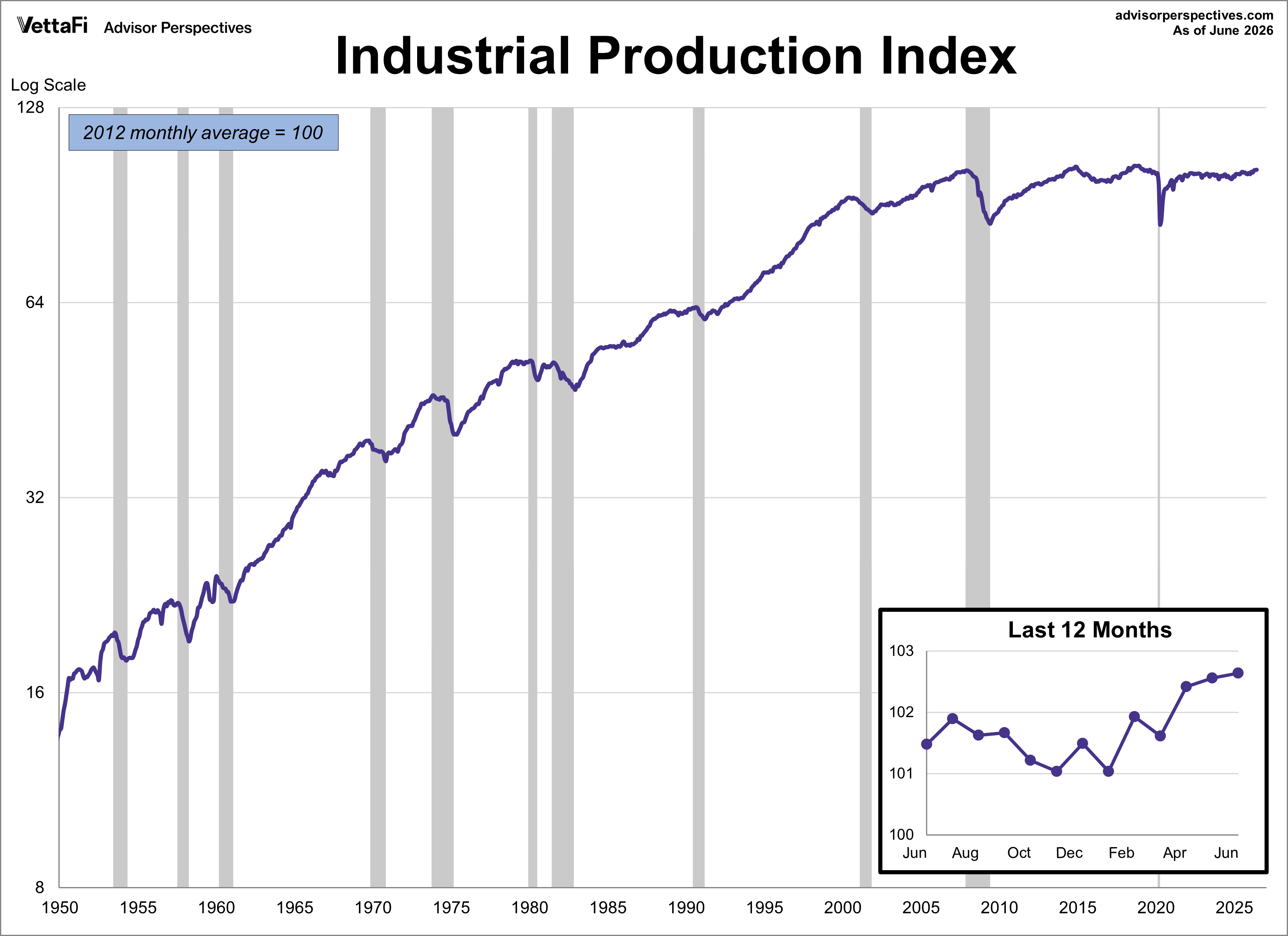

Industrial production measures the output of goods produced or mined in the U.S. While the manufacturing sector only makes up less than 20% of the economy, this indicator is closely watched as it is highly sensitive and quick to react to changes in the business cycle. The US industrial production Index (INDPRO) is the oldest of the four indicators, stretching back to 1919, although we've dropped the earlier decades and started in 1950.

In the charts below we have illustrated three different data manipulations:

- A log scale plotting of the complete data series to ensure that distances on the vertical axis reflect true relative growth. This adjustment is particularly important for data series that have changed significantly over time.

- A year-over-year representation to help, among other things, identify broader trends over the years. Industrial production year-over-year is currently below the level at the start of 8 of the 11 recessions that have started since 1950.

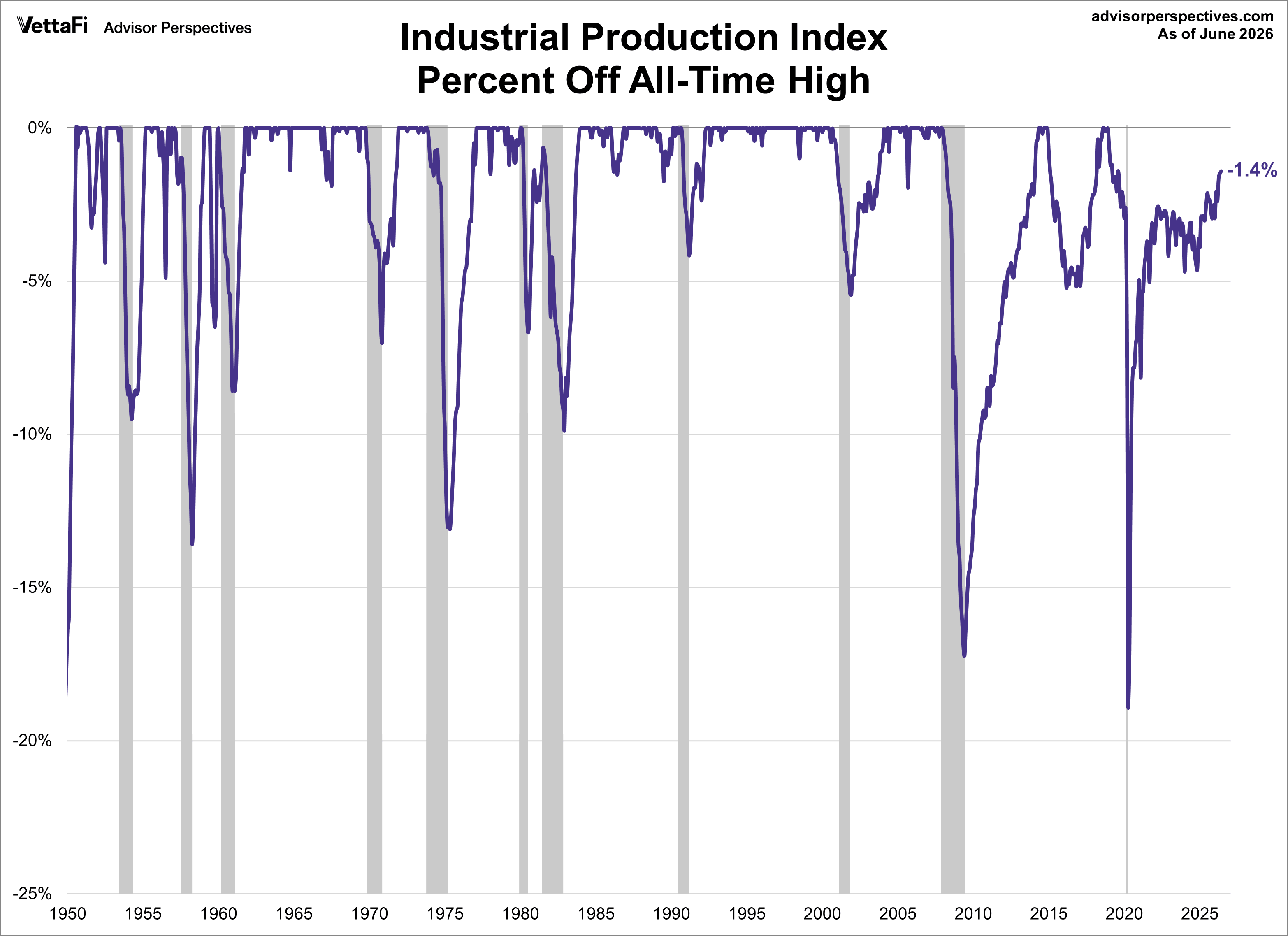

- A percent-off-high manipulation, which is particularly useful for better understanding of trend behavior and secular volatility. Industrial production is currently 1.4% off its all-time high from September 2018.

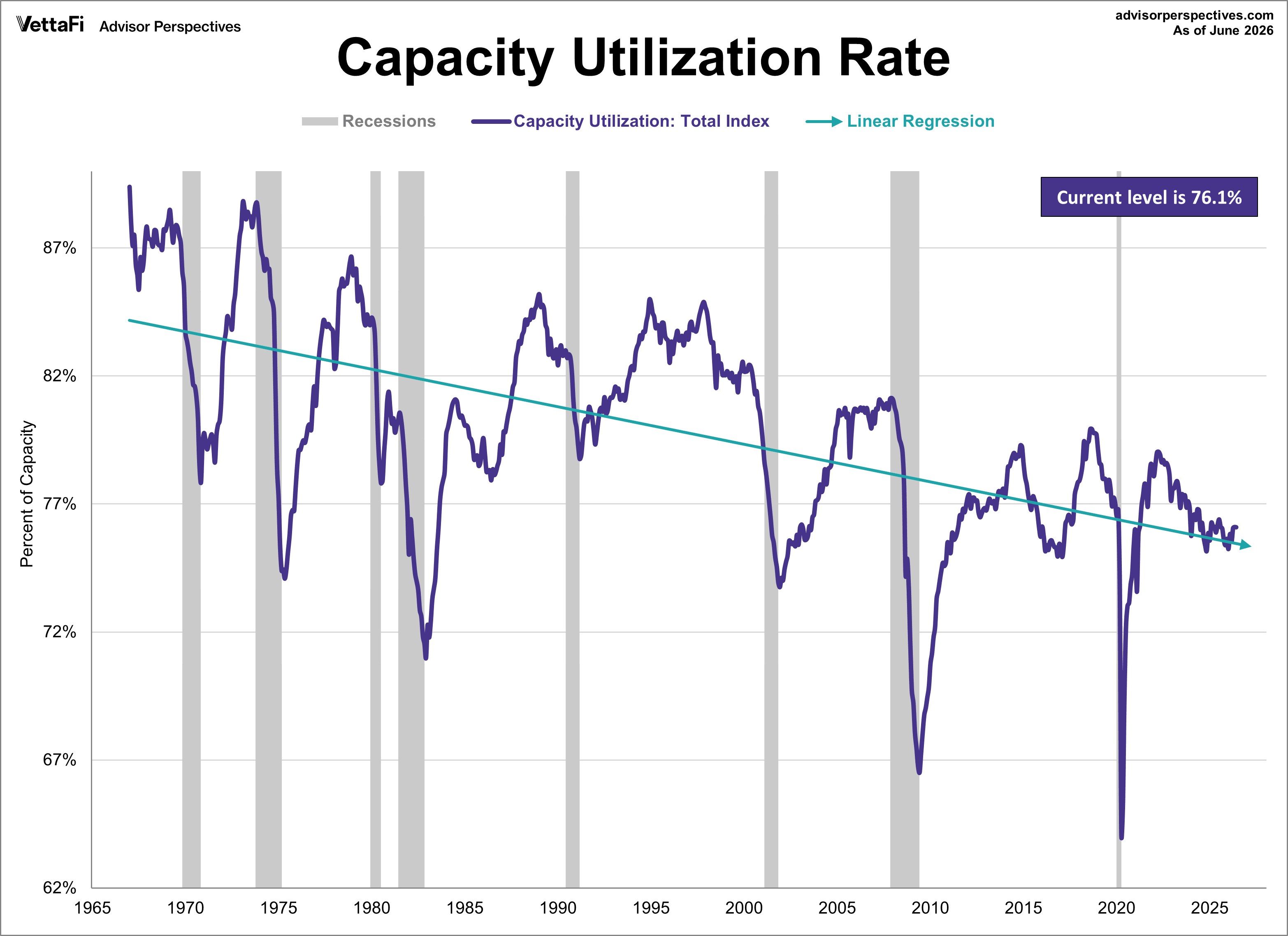

Industrial Production: Capacity Utilization

The Fed's monthly industrial production estimate is accompanied by another closely watched indicator, capacity utilization, which is the percentage of US total production capacity being used (available resources include manufacturing, mining, and electric and gas utilities). In other words, capacity utilization measures the amount of slack in the economy by looking at how much industries in the U.S. are presently producing and comparing that output to what they could potentially produce if the industrial sector was running at maximum capacity. In addition to showing cycles of economic growth and demand, capacity utilization also serves as a leading indicator of inflation because as American industry gets closer to operating at full capacity, shortages emerge which can generate inflation. When the economy is robust, the capacity utilization rate for manufacturing typically rises however when demand softens, the rate typically falls.

In June, the capacity utilization rate was at 76.1%, falling just short of the 76.2% forecast. This reflects a 0.0% monthly change and 0.1% annual decrease. Here is a chart of the complete capacity utilization series, which the Fed began tracking in 1967. The linear regression assists our understanding of the long-term trend. The 2022 peak is likely due in part to supply chain issues as a result of the COVID pandemic.

ETFs associated with industrial production include: Industrial Select Sector SPDR Fund (XLI), Vanguard Industrials ETF (VIS), and iShares U.S. Industrials ETF (IYJ).

Read more updates by Jen Nash